Downtown Orlando's 2026 commercial market is bifurcated: office is structurally weak with low-teens vacancy and negative absorption, while retail, hospitality, multifamily, self-storage, and medical office continue to generate durable cash flow. Florida-specific insurance, judicial-foreclosure, and doc-stamp drag must be modeled explicitly. Over $130 billion in Florida CRE loans mature between 2026 and 2030 — a maturity wall that will reshape Downtown ownership and create both REO and recapitalization opportunities for disciplined capital.

Why Downtown Orlando Still Matters for Serious Capital

Downtown Orlando is not Miami or Tampa — but for disciplined institutional capital, that's precisely the opportunity. The metro continues to post population and job growth, and Orlando's broader market shows strong fundamentals in retail, hospitality, and long-term multifamily demand even as capital markets remain cautious. At the metro level, average asking sale prices for commercial properties sit around the mid-$400s per square foot, with observed cap rates near 6.7%, offering a reasonable starting point for pricing risk in a post-zero-rate environment.

The catch is submarket dispersion. Downtown's office core is under pressure — with negative net absorption and elevated vacancy — while ground-floor retail, select hospitality, and urban multifamily still benefit from renewed activity and tourism-linked spending. For lenders and institutional buyers, Downtown Orlando today is a sorting mechanism: weak business plans, over-levered office, and undisciplined value-add stories are getting exposed, while well-located assets with realistic underwriting and durable tenancy are trading at a risk premium relative to coastal Florida.

Florida-specific headwinds — insurance repricing, judicial foreclosure timelines, and higher operating cost volatility — are forcing more conservative structures and lower leverage in Downtown Orlando than in the last cycle. If you treat this submarket like a generic Sunbelt growth story, you will misprice risk; if you underwrite like a credit officer and manage the downside, the spread over core coastal markets is meaningful.

Macro Tailwinds: Population, Tourism, and the I-4 Spine

At the macro level, Orlando remains one of the country's most resilient growth stories. Population growth, sustained in-migration, and a robust tourism engine continue to drive demand for multifamily, hospitality, and retail across the metro. Orlando's hotel market, for example, leads many top U.S. markets, with average daily rates recently reported above $230 and RevPAR up more than 20% year-over-year — numbers that flow directly into valuation for hospitality assets serving Downtown and nearby corridors.

The I-4 corridor — linking Tampa, Orlando, and Daytona — remains Florida's growth belt. Industrial vacancy across Florida often ranges in the mid-single digits — roughly 3.6–5.4% — with 15+ million square feet of annual absorption supported by e-commerce, logistics, and cold storage demand. While most of that square footage is not in Downtown proper, it underpins job growth and housing demand that bleed into the urban core, supporting multifamily, self-storage, and neighborhood retail near downtown.

Statewide commercial real estate loans totaling roughly $130+ billion are maturing between 2026 and 2030, with nearly half coming due in the next twenty-four months. That pipeline is not evenly distributed, but a slice of it sits on Downtown Orlando office, hospitality, and mixed-use projects financed at low cap rates and cheap debt. For community banks, credit unions, and private lenders with Downtown exposure, this is an early-warning system for non-performing loans and loan workouts that will shape pricing for years.

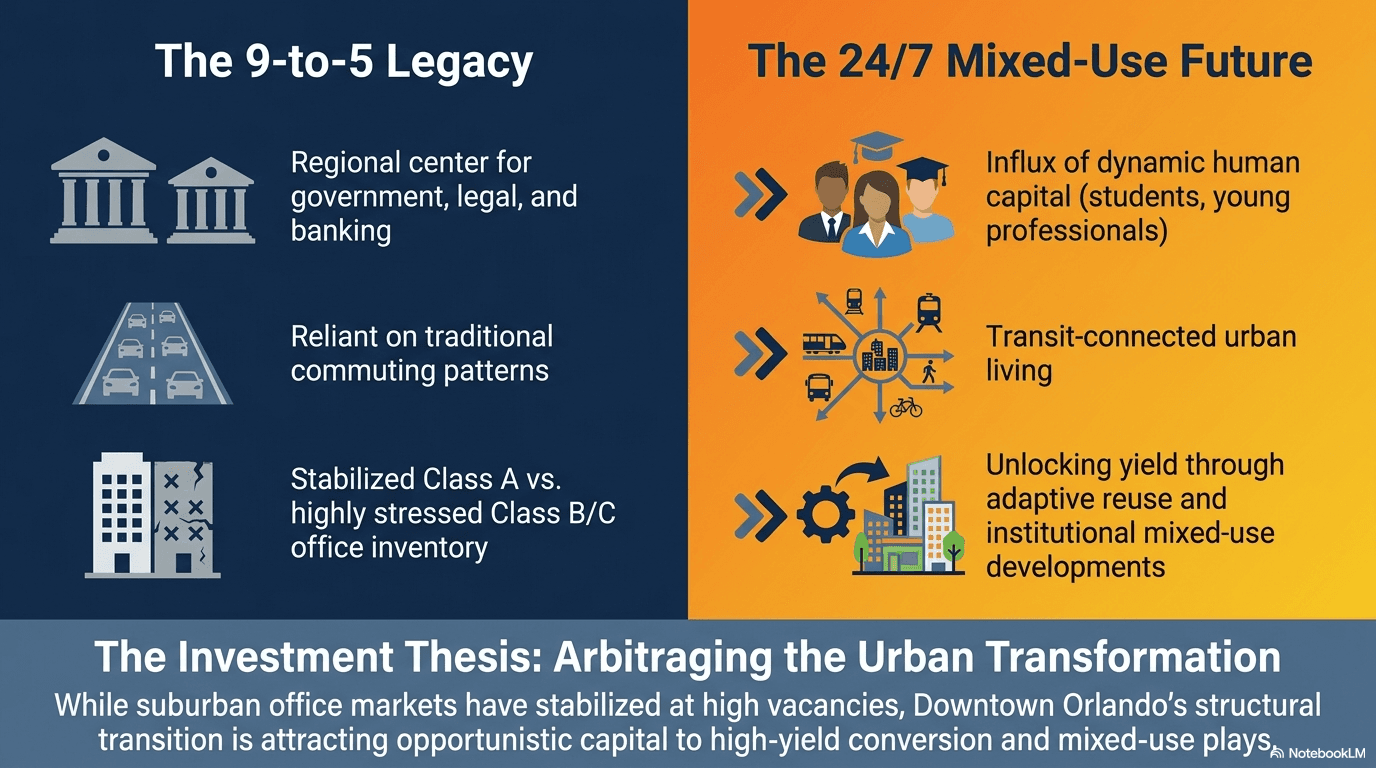

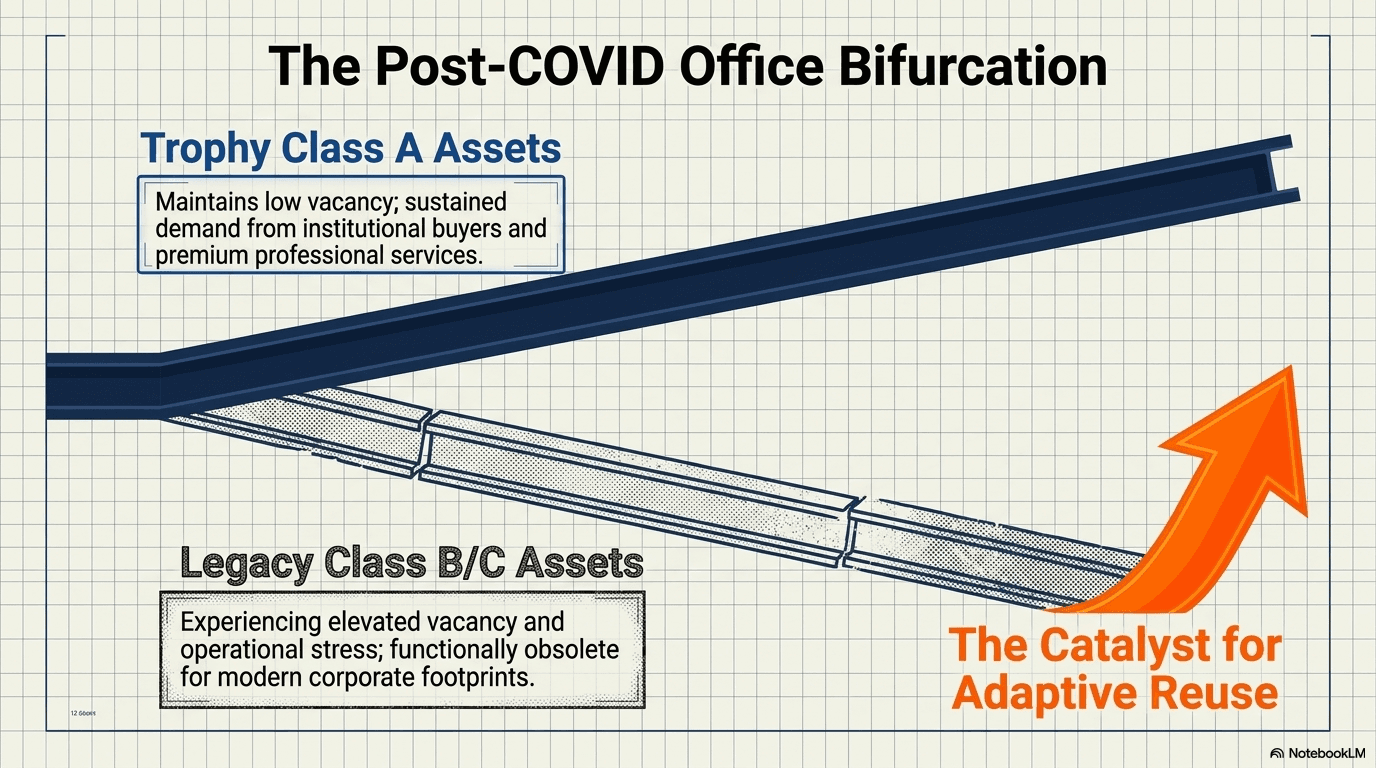

Downtown Orlando Office: Weak Link or Future Option Value?

The Downtown Orlando office market is still in a structural reset. Recent reports show downtown office vacancy near the low-teens — roughly 12–13% — with 12-month net absorption around negative 180,000 square feet, making it one of the weakest office cores in Florida by absorption. Sublease availability represents more than 10% of available sublease space in the Orlando region, highlighting how much shadow inventory is quietly competing with direct space.

Market rent growth in Downtown Orlando office has been slightly negative — around -0.3% — versus a 10-year average closer to 3.5%, with forecasts suggesting only low-single-digit positive rent growth as the market stabilizes. That is not a growth story; it is a credit and asset-management story. For lenders, this means underwriting with lower NOI and slower mark-to-market, and stress-testing DSCR against realistic lease-up timelines and re-tenanting costs. For equity, it means focusing on basis, optionality of conversion, and realistic exit cap rates instead of pro-forma rent spikes.

Yet there is a floor. Leasing activity is up more than 7% year-over-year and accounts for roughly 15% of all leasing volume in the Orlando metro, with high-profile tenants still willing to anchor best-in-class space. For institutional investors, this creates a bifurcated landscape: 4- and 5-star assets with strong sponsorship and credit tenancy may see mild repricing, while older B/C stock with major cap-ex needs, high operating cost exposure, and short weighted average lease terms will likely become candidates for REO, discounted note sales, or conversion strategies.

Multifamily and Urban Living: Normalization, Not Collapse

Orlando's multifamily story has shifted from explosive rent growth to disciplined normalization. After several years of 40%+ rent growth from 2020 to 2023 across Florida, annual rent gains have settled into the 2–4% range, and new supply is peaking through 2026. City-wide, stabilized occupancy levels around the mid-90s — roughly 94–95% — reflect a healthy but more competitive leasing environment as concessions creep back into select submarkets.

In and around Downtown Orlando — including adjacent zip codes such as 32803 — recent data shows average home values in the high $400,000s and median sold prices just under $500,000, with 6%+ year-over-year price gains and rising inventories. Median days on market have compressed into the twenty- to thirty-day range for well-positioned properties, suggesting that demand for urban living remains strong even as pricing moderates. For multifamily owners, this translates into steady demand but less aggressive rent growth than early-cycle projections assumed.

For institutional buyers and 1031 exchange capital, Downtown Orlando multifamily assets now look more like income vehicles than speculative appreciation plays. Underwriting needs to account for real insurance costs, realistic turnover, and higher operating expense ratios — especially in older mid-rise product — but the core demand drivers of population, jobs, and tourism remain intact. Deals that penciled only at 4% cap rates and 8% rent growth are gone; 5–5.75% cap rates with modest growth and some vacancy risk can still make sense if you buy well and fix operations.

Retail, Hospitality, and the Experiential Core

Orlando's retail market is one of the metro's bright spots. Recent data shows metro-wide retail vacancy around the mid-3% to low-4% range, with average asking rents near $30 per square foot and positive annual rent growth. Over the past year, nearly 800,000 square feet of new retail inventory has been delivered in the region with modest but positive net absorption — evidence of a healthy, not frothy, market. For Downtown Orlando, this manifests as strong demand for well-located ground-floor retail, food-and-beverage, and service uses tied to the courthouse, city government, and entertainment venues.

Hospitality is even stronger. Orlando's hotel market ranks among the top tier nationally, with average daily rates exceeding $230 and RevPAR growth in the 20%+ range as leisure and business travel continue to rebound. For Downtown hotels, select-service and lifestyle product positioned to capture both business and weekend entertainment demand is well-situated — though refinancing risk looms for assets levered at pre-2022 valuations. Lenders should underwrite using updated ADR, occupancy, and RevPAR assumptions, but also layer in higher debt yields and structural reserves for future cap-ex.

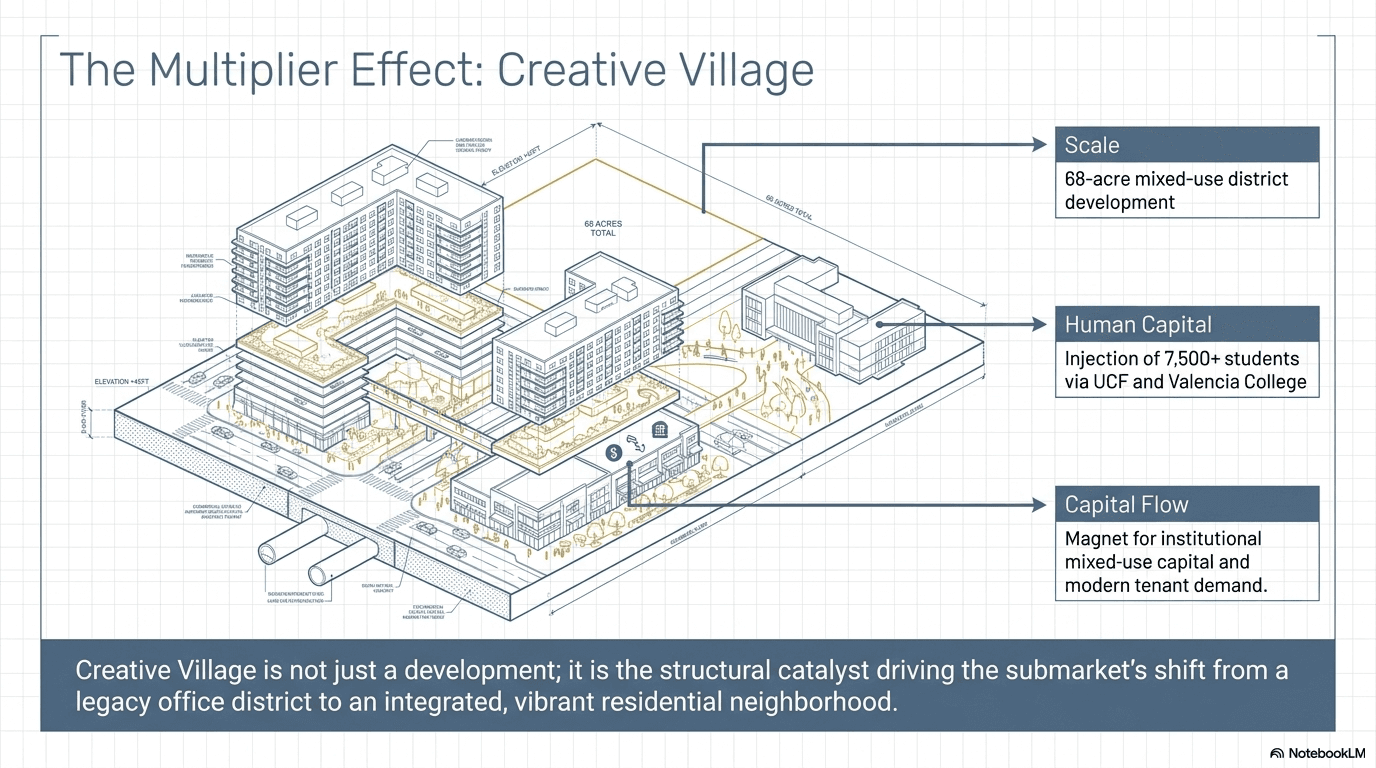

This dynamic favors mixed-use assets where retail and hospitality cash flows backstop weaker office or provide complementary income to multifamily above. It also creates a lane for community banks and private lenders willing to underwrite nuanced business plans rather than relying on generic global assumptions. With the right capital stack — often combining senior debt, preferred equity, and sponsor co-investment — Downtown Orlando experiential assets can still deliver attractive risk-adjusted yields.

Industrial, Self-Storage, and Edge-of-Core Opportunities

While you won't find large-format distribution centers in the middle of Downtown Orlando, the submarket benefits directly from Central Florida's industrial strength. Statewide industrial vacancy in the 3–5% range and double-digit annual absorption across the I-4 corridor support steady tenant demand and wage growth. This industrial engine drives demand for workforce multifamily, last-mile self-storage, and contractor-oriented flex space at the edges of downtown.

Self-storage and small-bay industrial remain compelling for lenders and private capital when underwritten properly. Low default histories, granular tenancy, and predictable operating expenses — subject, however, to Florida's insurance shock — make these asset classes attractive risk-weighted positions in an otherwise volatile environment. For Downtown Orlando, that often means conversions of obsolete buildings to climate-controlled storage or creative reuse as maker, flex, or hybrid retail-industrial space serving local trades and service providers.

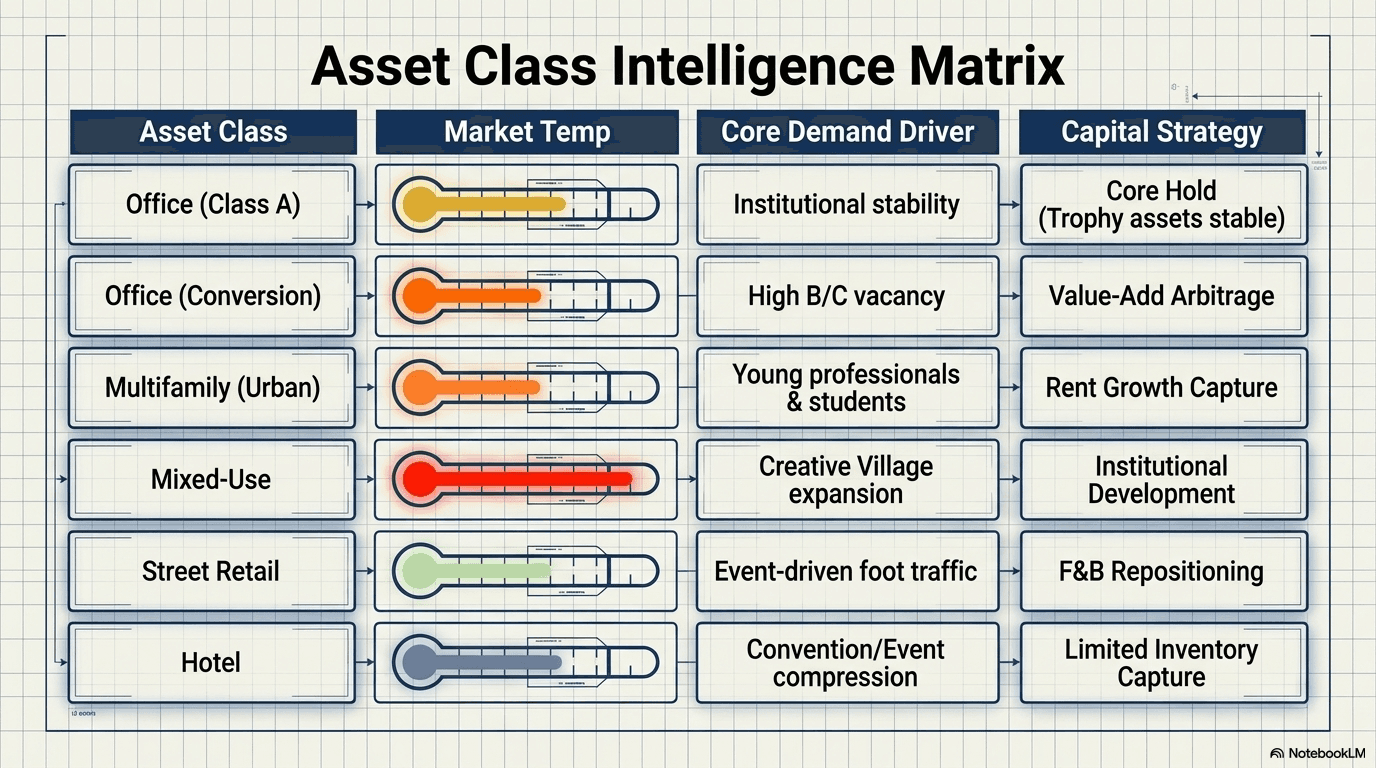

Asset Class Outlook — Downtown Orlando 2026

| Asset Class | Short-Term Outlook (12–24 mo) | Key Risk/Opportunity Driver |

|---|---|---|

| Office | Weak, selective opportunity | Negative absorption, conversion/REO optionality |

| Multifamily | Stable, normalized growth | 2–4% rent growth, supply peak 2026 |

| Retail | Strong, landlord-friendly | <4% vacancy, tourism-driven spending |

| Hospitality | Strong but refinancing risk | ADR > $230, RevPAR +20% YoY, higher debt costs |

| Self-Storage | Attractive, granular income | Industrial demand, population growth |

| Medical Office | Stable, defensive | Aging population, hospital affiliations |

| Land | Selective, entitlement-driven | Zoning, construction costs, capital markets |

Sources: Largo Capital, SunCoast SVN, NAR, Linton Global Solutions market analysis.

Florida-Specific Risk: Insurance, Judicial Foreclosure, and Doc Stamps

Any Downtown Orlando underwriting that does not explicitly model Florida-specific risk is incomplete. Property insurance costs across Florida have increased roughly 30–35% in recent years, with some markets seeing $3–5 per square foot or more added to operating expenses — directly compressing NOI and pushing cap rates higher. Coastal markets are hit hardest, but Orlando is not immune — hail, wind, and flood-adjacent risk still drive premium volatility and deductible creep. For office, multifamily, and hospitality assets, this can add 100–150 basis points of expense ratio vs. pre-2020 norms.

Florida's judicial foreclosure process adds another layer of complexity for community banks and credit unions. Timelines from first default to final judgment and sale can stretch into years depending on borrower defenses, backlog, and court capacity. That reality should shape loan structures, covenants, and reserve requirements up front — and drive proactive loan workout and note sale strategies before a file devolves into full litigation. When collateral is a Downtown Orlando office or mixed-use asset with uncertain re-tenanting prospects, time truly is the enemy of recovery.

Investors must also factor in documentary stamp tax on Florida real estate transfers and mortgage recordings, which adds non-trivial frictional cost on both acquisitions and refinancings. Coupled with flood/sinkhole risk in certain micro-markets — requiring careful Phase I ESA review, title insurance endorsements, and flood-zone analysis — these state and local dynamics directly impact levered yields. Done properly, they also create an edge for investors and lenders who actually understand them rather than underwriting to national averages.

A Downtown Orlando mid-rise multifamily asset with 120 units and 100,000 rentable square feet that sees insurance expense jump from $2.00 to $4.50 per square foot experiences a $250,000 annual NOI hit. At a 5.5% cap rate, that single line-item move can strip roughly $4.5 million from valuation — more than enough to turn a marginal refinance into a maturity default.

Capital Markets, Maturing Debt, and Silent Distress

Capital markets remain selective for Downtown Orlando. Nationwide, office and mixed-use lending standards have tightened, with lenders demanding higher debt yields and lower leverage while still pricing in regulatory and reserve requirements. In Florida specifically, a large concentration of commercial loans — over $130 billion statewide — is set to mature between 2026 and 2030, with nearly half maturing in the next two years. Downtown assets sitting on five- to seven-year loans underwritten at 2020–2021 assumptions are now facing an environment of higher rates, flat or negative rent growth in office, and higher expenses across the board.

For community banks and credit unions, this is where credit discipline will show. Files backed by Downtown office, hospitality, or transitional mixed-use must be triaged now — not at maturity. That means fresh valuations, rent rolls, and realistic pro-formas reviewed against your internal risk ratings and regulatory expectations. For sponsors, it means facing reality on equity gaps early and getting ahead of conversations about extensions, partial paydowns, or bridge loan solutions — rather than hoping for a rate miracle.

This is also the window where quiet distress and REO pipelines begin to form. Rather than waiting for full default and a protracted judicial foreclosure, many institutions will choose to sell non-performing loans, pursue consensual workouts, or recapitalize with new private equity partners. Downtown Orlando's mix of challenged office and solid underlying land value makes it a prime candidate for creative recapitalizations where basis reset and business plan reset happen simultaneously.

Get the next Florida CRE report.

Cap rates, absorption, distress watch — delivered when it ships. No spam.

Using REOMind.ai and Linton Global Solutions in Downtown Orlando

This is where process and tooling matter. Linton Global Solutions leverages REOMind.ai, a multi-agent AI platform, to create an institutional-grade view of Downtown Orlando assets in a fraction of the time a traditional team would need. The platform's Market Analyst Agent, Valuation Expert Agent, Compliance Monitor Agent, Investor Matcher Agent, and Risk Assessor Agent work together to automate the bulk of the heavy lifting across market analysis, valuation stress-testing, regulatory review, investor targeting, and downside scenario modeling.

For example, when evaluating a Downtown Orlando mixed-use property, the Market Analyst Agent can map real lease comps, rent trends, and vacancy by asset class along the I-4 corridor, while the Valuation Expert Agent runs multiple cap rate and NOI scenarios to test refinance and sale outcomes. The Compliance Monitor Agent flags potential regulatory, zoning, and environmental issues — including flood-zone or lien exposure — before they become closing problems, while the Risk Assessor Agent quantifies downside under higher insurance, expense, or vacancy assumptions.

For banks and credit unions, REOMind.ai can be pointed at a Downtown Orlando portfolio to identify which loans are most likely to become non-performing over the next 12–24 months, enabling proactive outreach and structured loan workout strategies instead of reactive loss mitigation. For institutional buyers and family offices, the Investor Matcher Agent can align specific risk/return targets with live and emerging opportunities in Downtown Orlando, Tampa, and the broader I-4 corridor — compressing the time from initial thesis to actionable deal flow.

Need a Real Downtown Orlando Underwriting Partner?

If you're an institutional investor, family office, or lender holding Downtown Orlando exposure, we can help you separate durable assets from future problems and structure capital accordingly.

Talk to Michael About Downtown Orlando →Execution Playbook for Institutional Investors and Lenders

For serious capital, Downtown Orlando in 2026 is not about chasing momentum — it is about precision. On the buy side, you focus on three things: basis, durability of cash flow, and exit liquidity. That means targeting well-located multifamily, retail, hospitality, self-storage, and medical office with realistic underwriting, while requiring deeper discounts and stronger structure to touch traditional office. Use conservative cap rate assumptions, underwrite flatter rent growth, and embed real insurance and tax loads rather than optimistic pro-formas.

On the credit side, banks and private lenders should segment Downtown exposure by asset quality and sponsor strength. Strong sponsors with high-quality collateral deserve structured solutions — extensions with covenants, partial paydowns, or rescue capital — while weak assets with weak sponsorship are better handled as early REO candidates or note sale opportunities. Align this triage with OCC and safety-and-soundness expectations so your internal and regulatory narratives stay consistent.

For both investors and lenders, the winning play is building repeatable decision systems — not one-off heroics. That is where working with a partner who combines local Florida expertise with AI-driven analytics matters. Downtown Orlando will reward those who do the unglamorous work: checking Phase I ESA details, reading leases instead of summaries, re-bidding insurance, and testing every deal against worst-case DSCR scenarios and multi-year exit paths.

Key Takeaways

Frequently Asked Questions

How high is Downtown Orlando office vacancy right now?

Recent reports show Downtown Orlando office vacancy around the low-teens — roughly 12–13% — with 12-month net absorption near negative 180,000 square feet and rising sublease availability. That puts Downtown among the weaker office submarkets in Florida by absorption, with only modest rent growth expected near term.

Is Downtown Orlando multifamily still a good bet for 1031 exchange buyers?

Yes — if you underwrite for normalized rent growth instead of the 2020–2022 surge. Metro-wide, multifamily rent growth has moderated to around 2–4% annually, with stabilized occupancy in the mid-90% range and pockets of supply-driven competition. For Downtown and adjacent zip codes, median pricing and quick days on market indicate continued demand, but returns are driven by income and operational efficiency, not speculative appreciation.

How are Florida insurance costs affecting Downtown Orlando commercial deals?

Property insurance costs across Florida have risen sharply — often 30–35% in recent years — with some assets seeing $3–5 per square foot added to annual operating expenses. In Downtown Orlando, that can wipe out hundreds of thousands in NOI on mid-size assets, expanding cap rates and shrinking loan proceeds if not proactively managed.

What asset classes look most compelling in Downtown Orlando over the next 24 months?

Well-located retail, hospitality, self-storage, and defensive medical office currently offer the best combination of demand visibility and pricing power, supported by low regional retail vacancy, strong tourism metrics, and industrial-driven population growth. Multifamily remains attractive as an income play, while traditional office demands deep discounts, strong business plans, or conversion potential to justify risk.

How should community banks manage maturing Downtown Orlando CRE loans?

Start triage early — well before maturity. Florida faces over $130 billion in CRE loan maturities statewide from 2026–2030, with nearly half due in the next two years, and Downtown Orlando office and mixed-use loans underwritten at pre-2022 assumptions are especially vulnerable. Banks should refresh valuations, rerun DSCR with current income and expenses, and pursue structured workouts, note sales, or recapitalizations before files devolve into protracted judicial foreclosures.

Where does REOMind.ai add the most value in Downtown Orlando underwriting?

REOMind.ai adds the most value where speed and depth intersect — portfolio triage, distressed asset evaluation, and institutional-grade underwriting of complex Downtown Orlando properties. Its multi-agent system can automate market analysis, valuation scenarios, regulatory and environmental checks, investor targeting, and risk scoring for hundreds of assets in the time a traditional team could fully underwrite only a handful.

I've been working Downtown Orlando and the broader I-4 corridor long enough to see multiple cycles and more than a few “can't-miss” stories turn into loan workouts. The investors and lenders who win here are the ones who underwrite like credit officers and stay brutally honest about risk. If you bring that mindset to Downtown Orlando today, there is still very real opportunity.

— Michael R. Linton, FL Broker #BK703722, NCREA, CREIPS, REALTOR®, 39 years Florida CRE

Works Cited

- City of Orlando. “City of Orlando Market Report.” orlando.gov, https://www.orlando.gov

- Matt Gillis. “Orlando Commercial Real Estate Outlook: Retail Growth, Multifamily Shifts, Hospitality Surge.” largocapital.com, https://largocapital.com/orlando-commercial-real-estate-outlook-2025/

- SunCoast SVN. “Office Reset in Real Time: Inside Downtown Orlando's Market Shift.” suncoastsvn.com, https://suncoastsvn.com/downtown-orlando-office-market-update-q3-2025/

- Michael R. Linton. “Florida Commercial Real Estate Market Report 2026.” hiremikelinton.com, https://hiremikelinton.com/florida-cre-market-report

- National Association of Realtors. “Commercial Real Estate Market Insights.” nar.realtor, https://www.nar.realtor/research-and-statistics/research-reports