Why Florida CRE Closings Cost More Than You Think

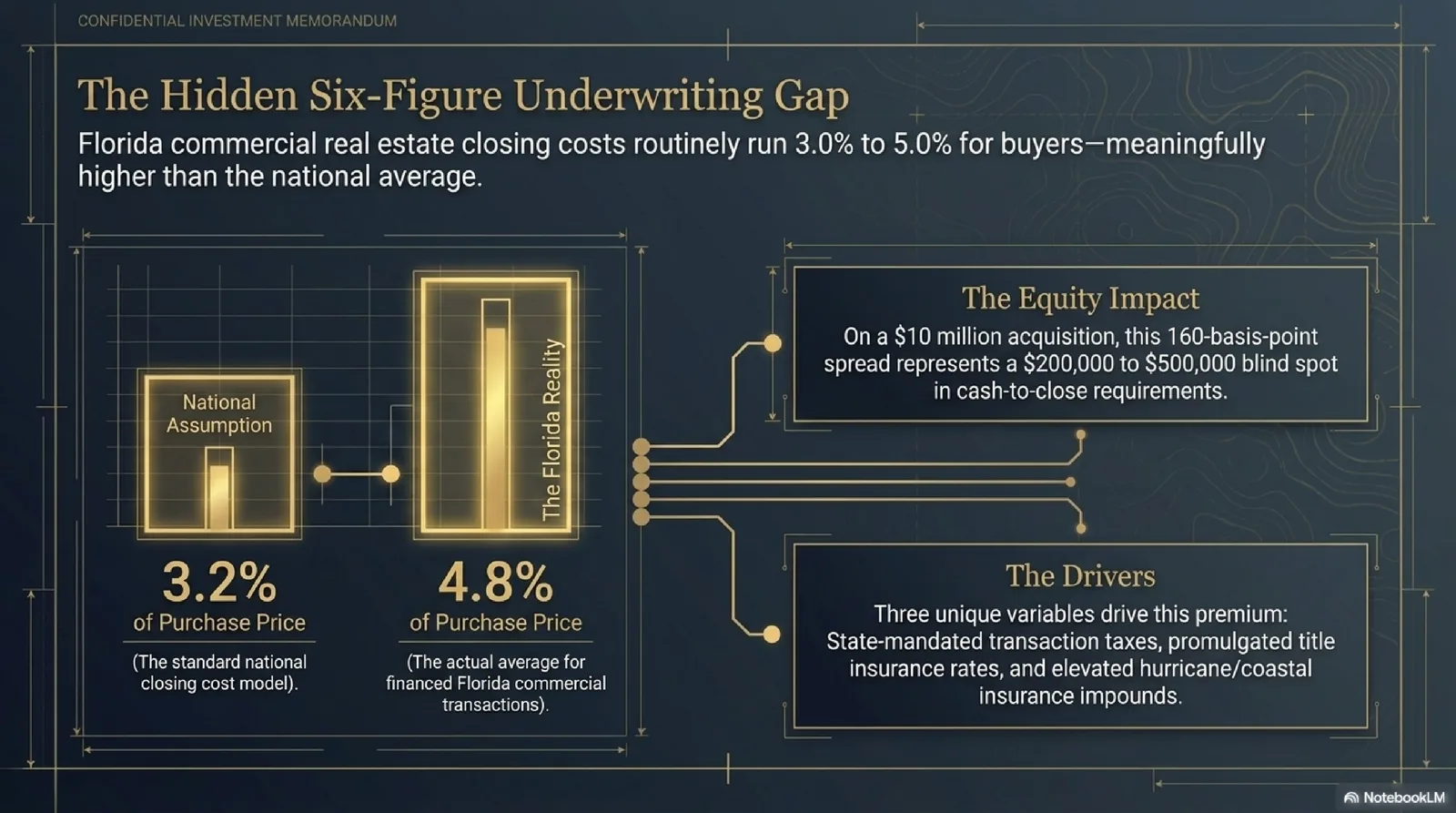

Florida commercial real estate closing costs routinely run 3–6 percent of purchase price for buyers — and 6–9 percent for sellers once brokerage commissions are included — making the state one of the more expensive closing environments in the country. The national average buyer closing cost is roughly 3.2 percent of the purchase price, while Florida averages around 4.8 percent, and commercial deals layer on costs that residential transactions never see: full ALTA/NSPS surveys, Phase I ESAs, zoning endorsements, and double state-level taxation on both the deed and the mortgage note.

For an institutional investor closing on a $10 million Florida multifamily or industrial deal, that spread between assuming “standard” closing costs and modeling the real Florida-specific stack can represent anywhere from $200,000 to $500,000 in additional cash needed at closing — a difference large enough to change a deal's equity structure.

REOMind.ai's pre-contract underwriting phase explicitly models all of these costs before a bid is submitted, preventing the all-too-common outcome of a deal that works at the bid price but breaks at the closing table. For community banks managing REO dispositions or institutional buyers sourcing NPL portfolios, accurate closing cost modeling is not a courtesy — it is a fundamental part of the risk-adjusted return calculation.

Documentary Stamp Tax: Florida's Big Revenue Line

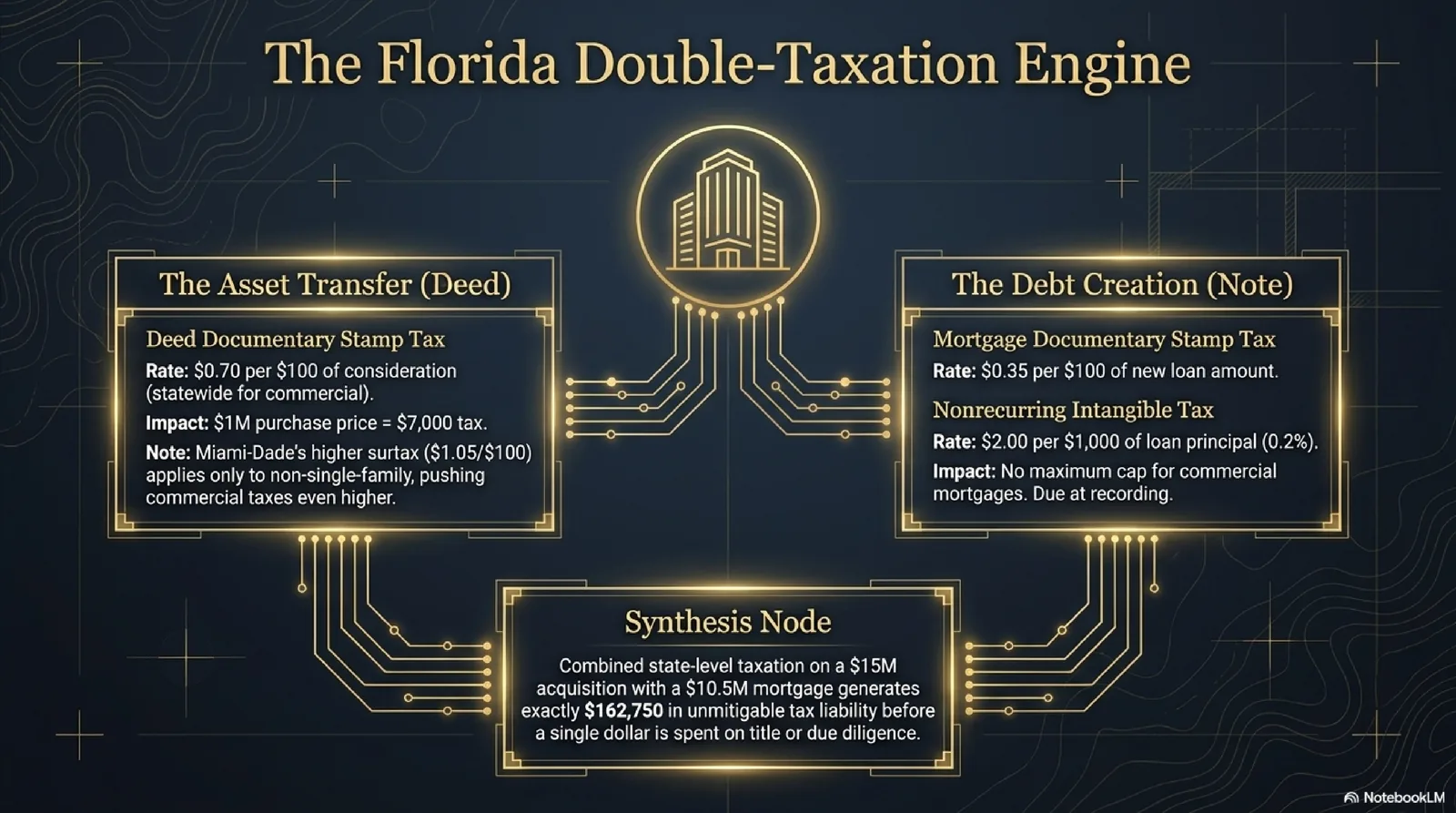

Documentary stamp tax is the single largest state-mandated closing cost in most Florida commercial transactions. Under Florida Statutes Chapter 201, Florida imposes a doc stamp tax at the rate of $0.70 per $100 of consideration on deeds transferring real property — meaning every $1 million of purchase price generates $7,000 in documentary stamp tax on the deed. Miami-Dade County is the notable exception: for non-single-family-residence transactions, the rate is $0.60 per $100 plus a surtax of $0.45 per $100, producing a combined rate of $1.05 per $100 — or $10,500 per $1 million.

A second, separate documentary stamp tax applies to the promissory note itself. Under Florida Statutes Section 201.08(1), the tax on mortgages, notes, and other written obligations to pay money is $0.35 per $100 of the amount financed. For a $7 million commercial mortgage financing a $10 million acquisition, that produces $24,500 in documentary stamp tax on the note, in addition to the $70,000 on the deed — a combined hit of $94,500 in doc stamps alone.

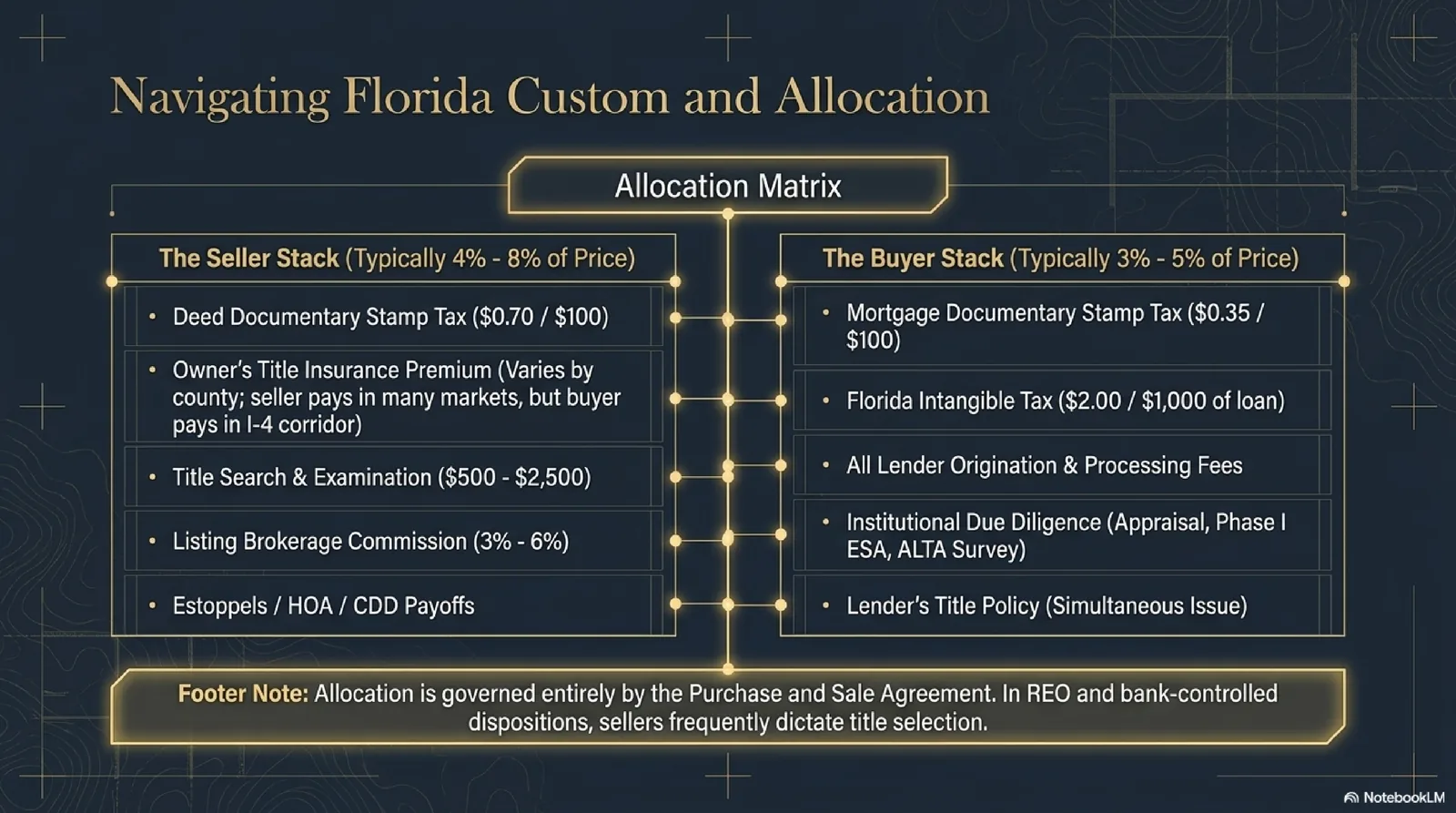

In practice, documentary stamp tax on the deed is typically a seller obligation in most Florida commercial purchase agreements, while documentary stamp tax on the note is a buyer obligation paid at closing through the title company. However, this allocation is not mandated by Florida law — it is negotiated between the parties and governed entirely by the purchase and sale agreement.

- Doc stamp tax on deed (seller-side): $105,000

- Doc stamp tax on note (buyer-side): $36,750

- Nonrecurring intangible tax on mortgage (buyer-side): $21,000

- Combined state-level taxation: $162,750

This is before a single dollar of title, survey, appraisal, or lender fees.

Nonrecurring Intangible Tax on Mortgages

Florida's nonrecurring intangible tax is a one-time state levy on mortgages and other obligations to pay money secured by Florida real property. Under Florida Statutes Section 199.133, the rate is 2 mills — $2.00 per $1,000 of the mortgage amount, or equivalently, 0.2 percent of the loan principal. Unlike documentary stamp tax on notes, the nonrecurring intangible tax carries no maximum cap for commercial mortgages.

For a $25 million mortgage on a Florida multifamily or industrial acquisition, the intangible tax is $50,000 — a line item that can surprise borrowers who come from states with no analogous tax. The tax is due and payable at the time the mortgage is recorded with the county clerk — it cannot be financed into the loan or deferred.

For bridge-loan financing on transitional assets, or construction loans with future advance provisions, the intangible tax is calculated on the full face amount of the mortgage — not just the amount outstanding at closing. This means a $20 million construction loan generates a $40,000 intangible tax obligation at the initial draw, even if only $5 million is advanced at closing.

Get the next Florida CRE report.

Cap rates, absorption, distress watch — delivered when it ships. No spam.

Title Insurance: Rates, Who Pays, and What You Are Buying

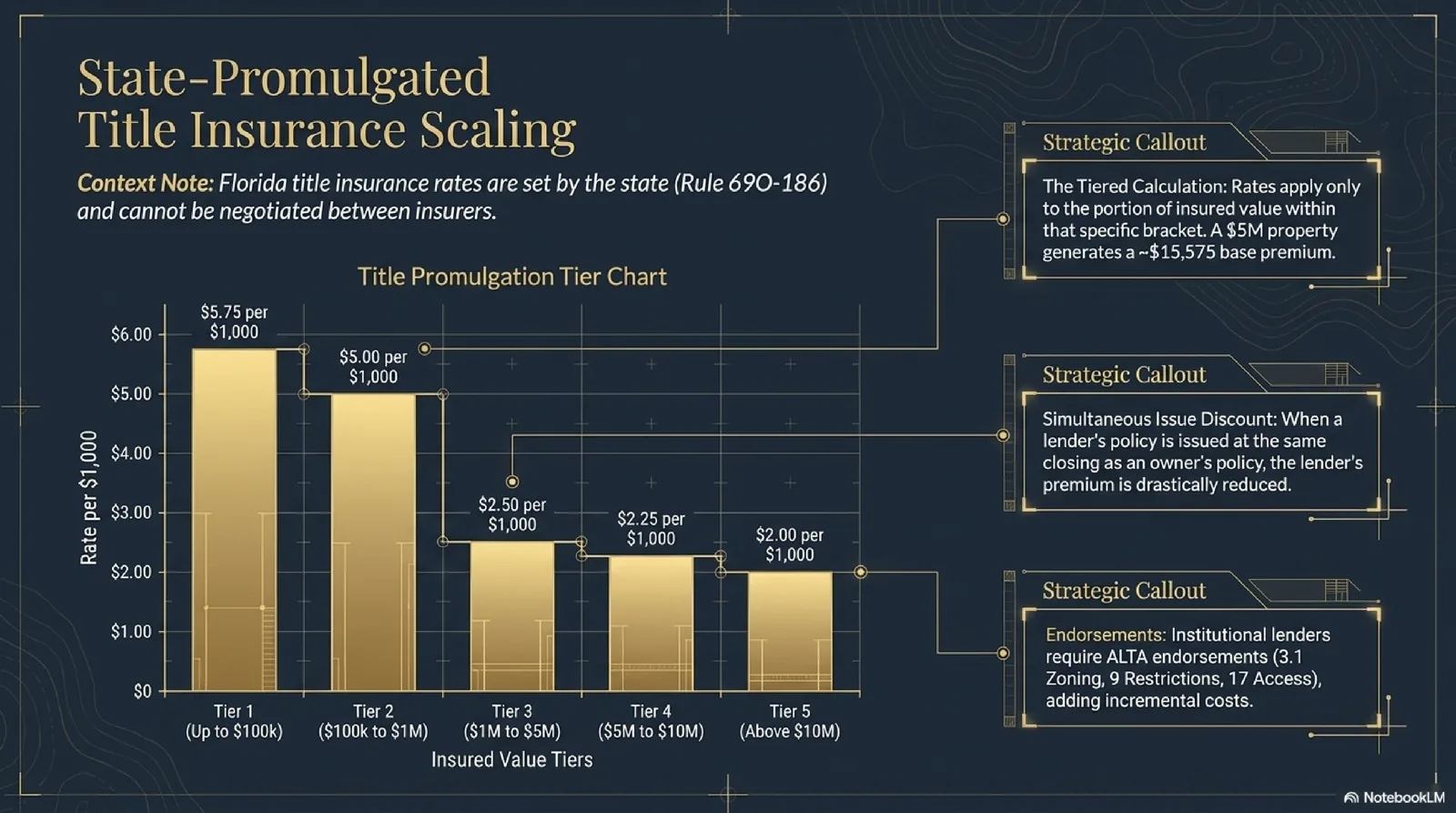

Florida's title insurance rates are set by the state and are not negotiable between insurers. The state promulgated schedule is: $5.75 per $1,000 on the first $100,000, $5.00 per $1,000 on the next $900,000, $2.50 per $1,000 from $1M to $5M, $2.25 per $1,000 from $5M to $10M, and $2.00 per $1,000 above $10M. A $5 million commercial property generates approximately $12,500 in owner's title insurance premium, and a $10 million deal generates roughly $25,000.

Commercial transactions with lender financing require a separate lender's title insurance policy. In Florida, a simultaneous issue discount applies when both policies are issued at the same closing — the lender's policy is issued at a significantly reduced premium. Beyond the base premium, lenders regularly require ALTA endorsements — including the ALTA 3.1 for zoning, ALTA 9 for restrictions and encroachments, ALTA 17 for access, and environmental-lien endorsements.

Who pays for title insurance in Florida varies by county custom and by contract negotiation. In most Florida counties including Orange, Osceola, Polk, and Hillsborough (the core I‑4 corridor markets), the buyer typically selects the title company and pays for the owner's policy. On REO and bank-controlled dispositions, the seller-bank often insists on choosing the title company.

The ALTA/NSPS Survey: What It Covers and What It Costs

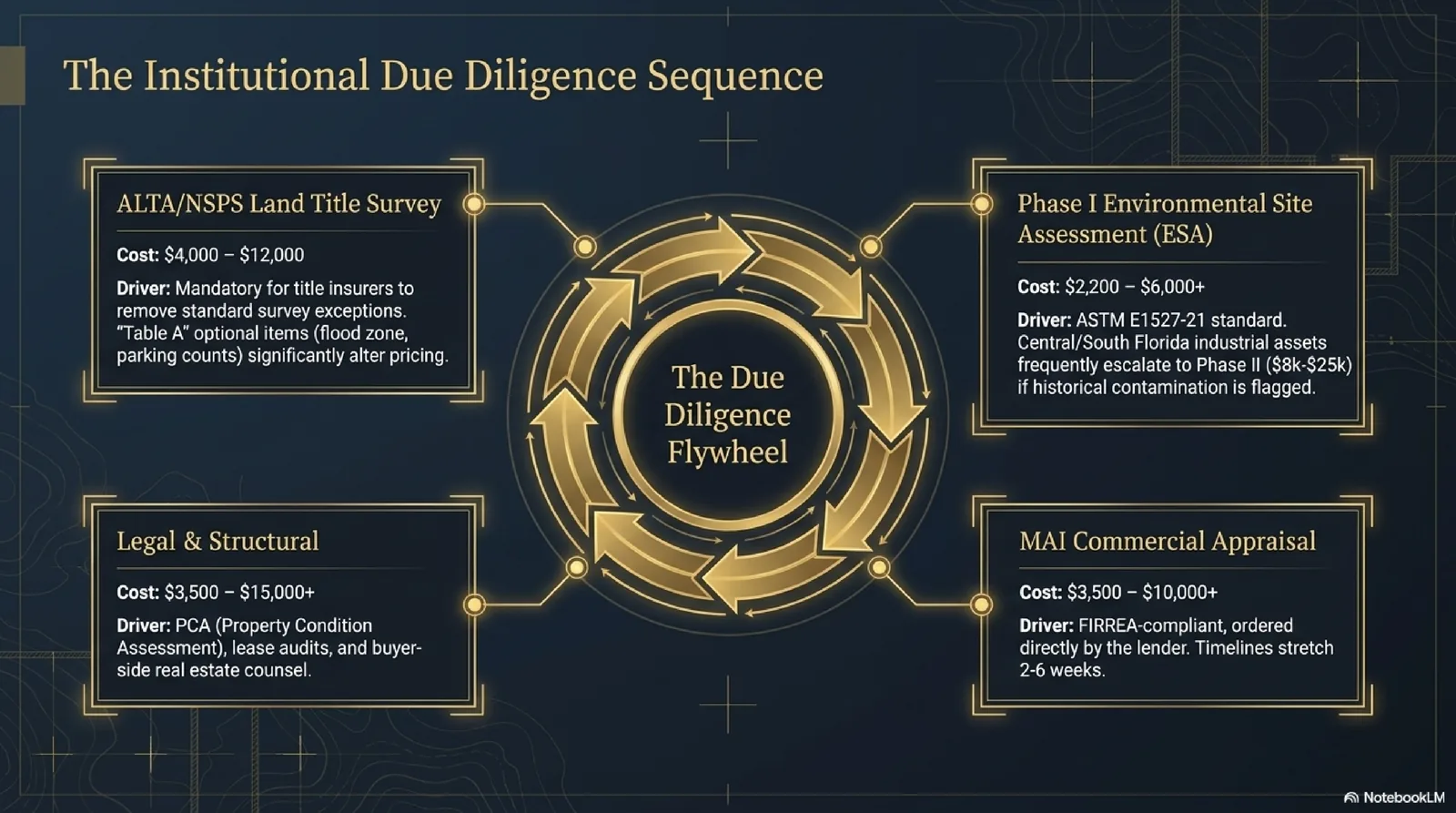

A full ALTA/NSPS Land Title Survey is effectively mandatory on any institutionally financed commercial real estate transaction. Lenders require it because title insurers use it to remove standard survey-related exceptions from the owner's and lender's policies.

ALTA survey costs in Florida depend on property size, complexity, the number of optional “Table A” items required by the lender, and turnaround time. National data for the Southeast region shows ranges of $4,000–$12,000 for most standard commercial deals, with smaller simple sites starting around $2,500 and large multi-acre assemblages reaching $25,000 or more. In Orlando, ALTA survey costs run roughly three percent above national averages, with standard deals ranging from approximately $3,245 to $8,652 for a two-to-three week turnaround — and rush service adding 25–100 percent.

Table A optional items significantly affect cost. Flood zone determination (Table A Item 2), parking counts (Item 6), utilities (Item 1), and adjoining owner identification (Item 13) are commonly required by lenders on multifamily, industrial, and retail deals in the I‑4 corridor.

Phase I ESA: Environmental Due Diligence

A Phase I Environmental Site Assessment is required by virtually every institutional lender under the ASTM E1527-21 standard. The Phase I reviews historical land use, aerial photographs, government records, and site conditions to identify any Recognized Environmental Conditions (RECs) that could signal contamination.

Phase I ESA costs in Florida range from $1,500–$2,500 for low-risk small sites, $2,000–$4,000 for standard commercial properties, and $4,000–$6,000+ for high-risk or large industrial sites, with complex brownfields or former gas stations potentially exceeding $7,500–$10,000. For former dry cleaners, auto repair shops, or older industrial uses common in some I‑4 corridor submarkets, buyers should budget toward the high end and allow an extra 2–4 weeks.

The cost of getting this wrong is orders of magnitude larger than the cost of a Phase I. Florida's FDEP can compel cleanup at properties with confirmed contamination, and cleanup costs can easily run into seven or eight figures on large industrial sites. REOMind.ai's Risk Assessor Agent flags properties with high ESA risk based on prior industrial use, proximity to known contamination sites, and property age.

Commercial Appraisal: Cost, Timeline, and Lender Requirements

Every institutionally financed commercial acquisition in Florida requires a FIRREA-compliant appraisal ordered directly by the lender — not the borrower. Commercial appraisal costs range from $2,000–$5,000 for small office, retail, or self-storage assets, to $5,000–$10,000+ for larger multifamily, industrial, hospitality, and medical office properties. Completion time is 2–6 weeks for standard lender work, but can extend to 2–6 months for complex assignments.

One of the most common underwriting mistakes on commercial deals is confusing the “as-is” appraised value with the “as-stabilized” value. Lenders typically lend off “as-is” unless there is a structured holdback, which affects both the DSCR calculation and the amount available to borrow at closing. REOMind.ai's Valuation Expert Agent cross-references lender appraisals against its own CREDDS scoring, flagging cases where a bank appraisal is above or below what market transaction data would support.

Lender Fees: Origination, Underwriting, and Processing

Commercial mortgage lender fees are higher than residential norms and less standardized. A typical loan origination fee runs 0.5–1.0 percent of the loan amount, plus separate underwriting ($1,500–$3,000), processing ($500–$1,500), and loan commitment fees ($1,000–$5,000+). For bridge or hard money financing, origination fees can climb to 1.5–3.0 percent, and some lenders charge an additional exit fee at payoff.

Bridge and construction lenders also typically require: (1) a commitment fee paid upfront, (2) an interest reserve built into the loan structure to cover initial months of NOI ramp-up, and (3) a rate lock fee if the borrower wants to protect against rate changes during the application period.

Recording Fees, Closing Fees, and Often-Forgotten Line Items

Florida county recording fees are modest individually but add up on complex commercial transactions. The base recording fee in most Florida counties is $10 for the first page and $8.50 for each additional page. A commercial deed, mortgage, assignment of leases, UCC financing statement, and survey plat can collectively run 40–100 pages, generating $350–$1,000+ in recording fees.

Title company settlement fees for commercial transactions typically run $1,500–$3,500, with higher fees for REO, distressed, multi-party, or 1031 closings. Document preparation fees run an additional $400–$600.

Often-forgotten but easily totaling $2,000–$10,000: wire transfer fees ($25–$50 each, with multiple wires common), HOA estoppel letters ($250–$500 per association), lien search fees ($100–$300 per county), flood certificates ($20–$50), and courier fees for original recorded documents.

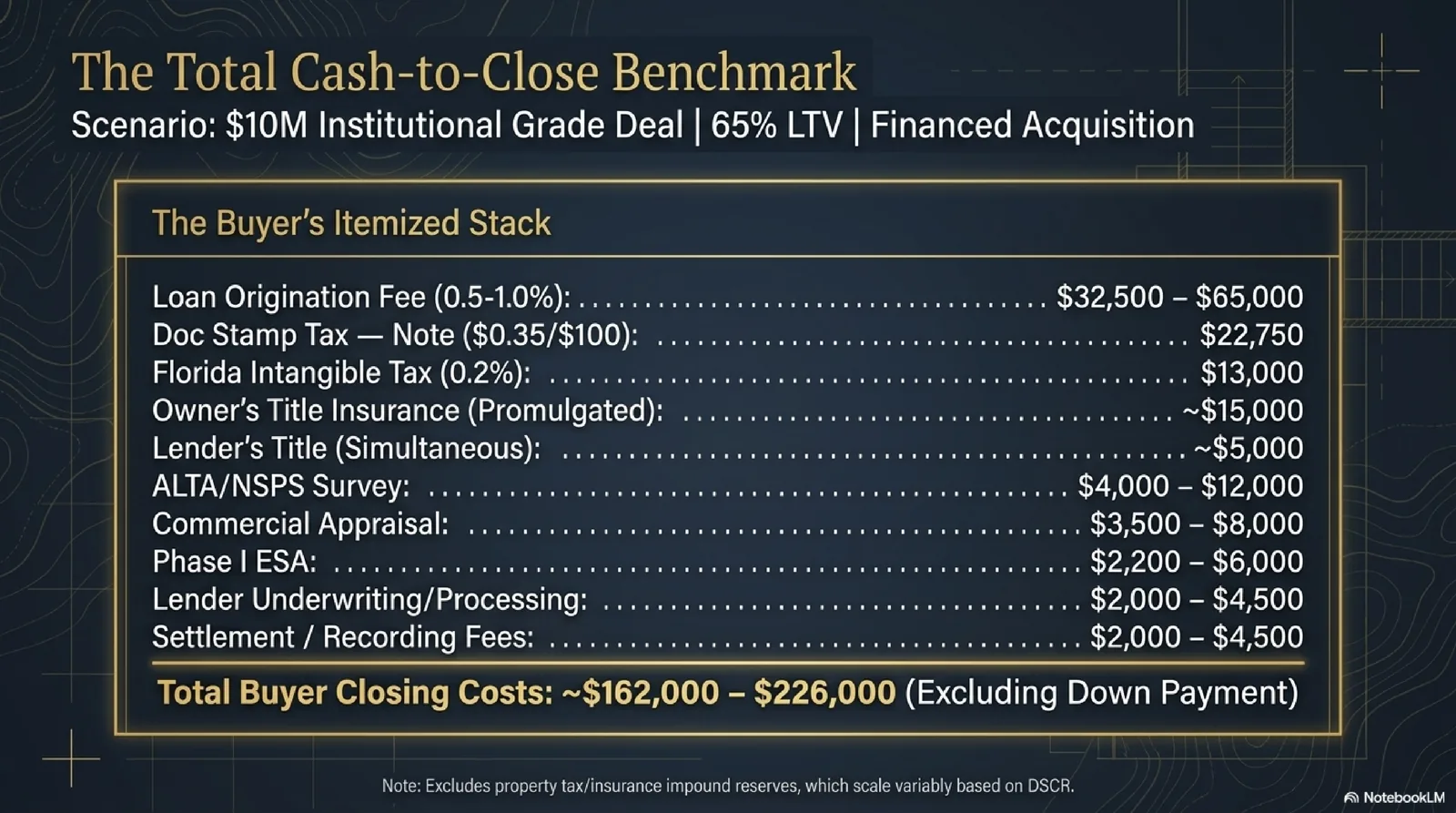

Closing Cost Benchmark — $10M Deal, 65% LTV

| Line Item | Rate / Basis | Est. Cost |

|---|---|---|

| Doc Stamp — Deed (seller, for ref.) | $0.70/$100 of price | $70,000 |

| Doc Stamp — Note (buyer) | $0.35/$100 of loan | $22,750 |

| Intangible Tax (buyer) | 0.2% of loan | $13,000 |

| Owner's Title Insurance | FL State Filed Rate | ~$15,000 |

| Lender's Title (simultaneous) | Discounted rate | ~$5,000 |

| ALTA/NSPS Survey | Property-specific | $4,000–$12,000 |

| Phase I ESA | Site type-specific | $2,200–$6,000 |

| Commercial Appraisal | Asset class-specific | $3,500–$8,000 |

| Loan Origination Fee | 0.5–1.0% of loan | $32,500–$65,000 |

| Lender Underwriting/Processing | Flat fee | $2,000–$4,500 |

| Settlement / Closing Fee | Flat fee | $1,500–$3,500 |

| Recording Fees | Per-page county rate | $500–$1,000 |

| Buyer Total (excl. down payment) | ~3.0–5.0% of price | ~$162,000–$226,000 |

Seller-Side Closing Costs and Broker Commissions

From the seller's perspective, Florida commercial closing costs generally run 4–8 percent of the sale price, with brokerage commissions representing the largest component. A standard commercial brokerage commission in Florida ranges from 3–6 percent, depending on deal size, asset type, and whether a buyer's broker is compensated. On a $10 million transaction with a 4 percent total commission, that is $400,000 before any other closing cost.

Documentary stamp tax on the deed — $70,000 on that same $10 million sale outside Miami-Dade — is typically a seller cost in Florida per local market custom. Sellers also typically pay prorated property taxes and assessments through the closing date, and any outstanding lien or municipal obligations discovered in the pre-closing search. For REO sellers, outstanding real estate taxes, insurance arrears, HOA fees, code enforcement liens, and unpaid utilities must all be cleared through closing or negotiated as buyer credits.

One category sellers often overlook: the documentary stamp tax on any seller financing. If a seller agrees to carry back $2 million at 7 percent interest, a doc stamp tax of $7,000 is due on that promissory note at closing, plus an additional $4,000 in intangible tax on the secured obligation.

1031 Exchange Closing Costs: Additional Complexity, Real Dollars

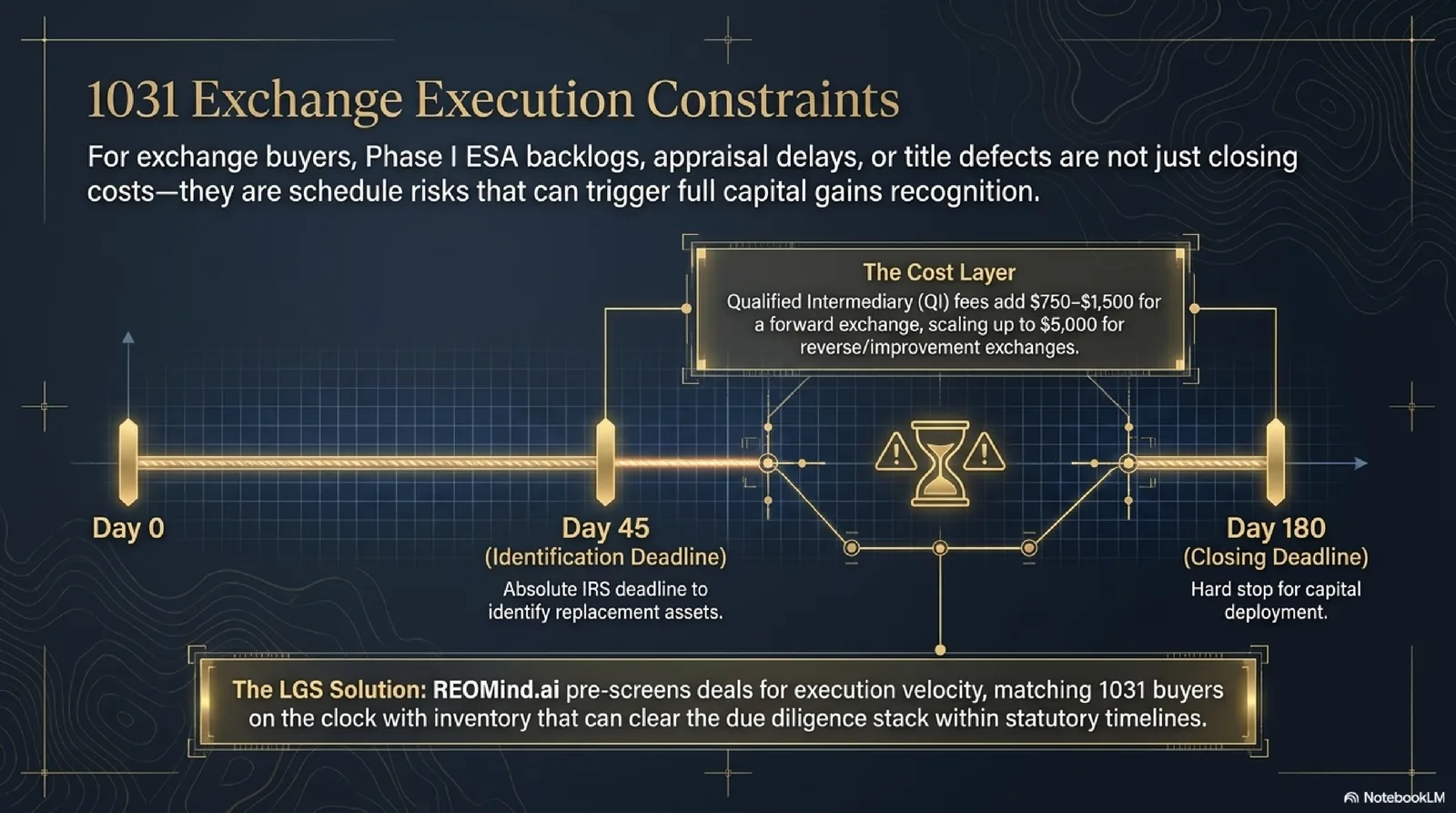

1031 exchange transactions add a layer of cost and coordination that buyers and sellers on the I‑4 corridor must model explicitly. The qualified intermediary (QI) fee typically runs $750–$1,500 for a basic forward exchange, rising to $2,500–$5,000 for a reverse or improvement exchange. These fees are in addition to all standard closing costs on both the relinquished and replacement property transactions.

On the replacement property closing, the buyer-exchanger faces the full stack of Florida closing costs — same as any other buyer, with one additional constraint: timing. The 45-day identification deadline and 180-day closing deadline under IRC Section 1031 are absolute, which means a Phase I ESA taking six weeks, an appraisal backlog at the lender, or a title defect requiring a quiet title action can blow the exchange and trigger full recognition of the capital gain.

REOMind.ai's Investor Matcher Agent specifically screens the 15,000-investor database for 1031 exchange buyers who have active exchange proceeds on the clock — matching their required closing timeline, basis requirements, and asset class preferences against available inventory.

Due Diligence Deposits, Escrow Structure, and Proration Math

Commercial Florida purchase agreements typically call for an initial earnest money deposit of 1–3 percent of the purchase price, deposited into escrow within three to five business days of contract execution. A second deposit — often bringing the total to 3–5 percent — may be due at the expiration of the due diligence period, and this second deposit is typically fully non-refundable. On distressed REO sales, banks often require a fully hard deposit from day one.

Property tax prorations in Florida are calculated based on the current-year calendar (January 1 through December 31), with taxes payable in arrears. Florida real estate taxes are due in full by March 31 of the following year, with a 4 percent discount for November payment, 3 percent for December, 2 percent for January, and 1 percent for February. On recently transacted properties, the assessed value may step up significantly at next reassessment, creating a budget gap the buyer's pro forma should anticipate.

On REO acquisitions of assets that have been insurance-dark during the foreclosure period, the buyer must also budget for binding new coverage at closing — and in Florida's current insurance market, this can be a shock for inland properties and a genuine deal-killer on some coastal assets.

DSCR and Florida Commercial Closing Costs: How the Ratio Drives the Stack

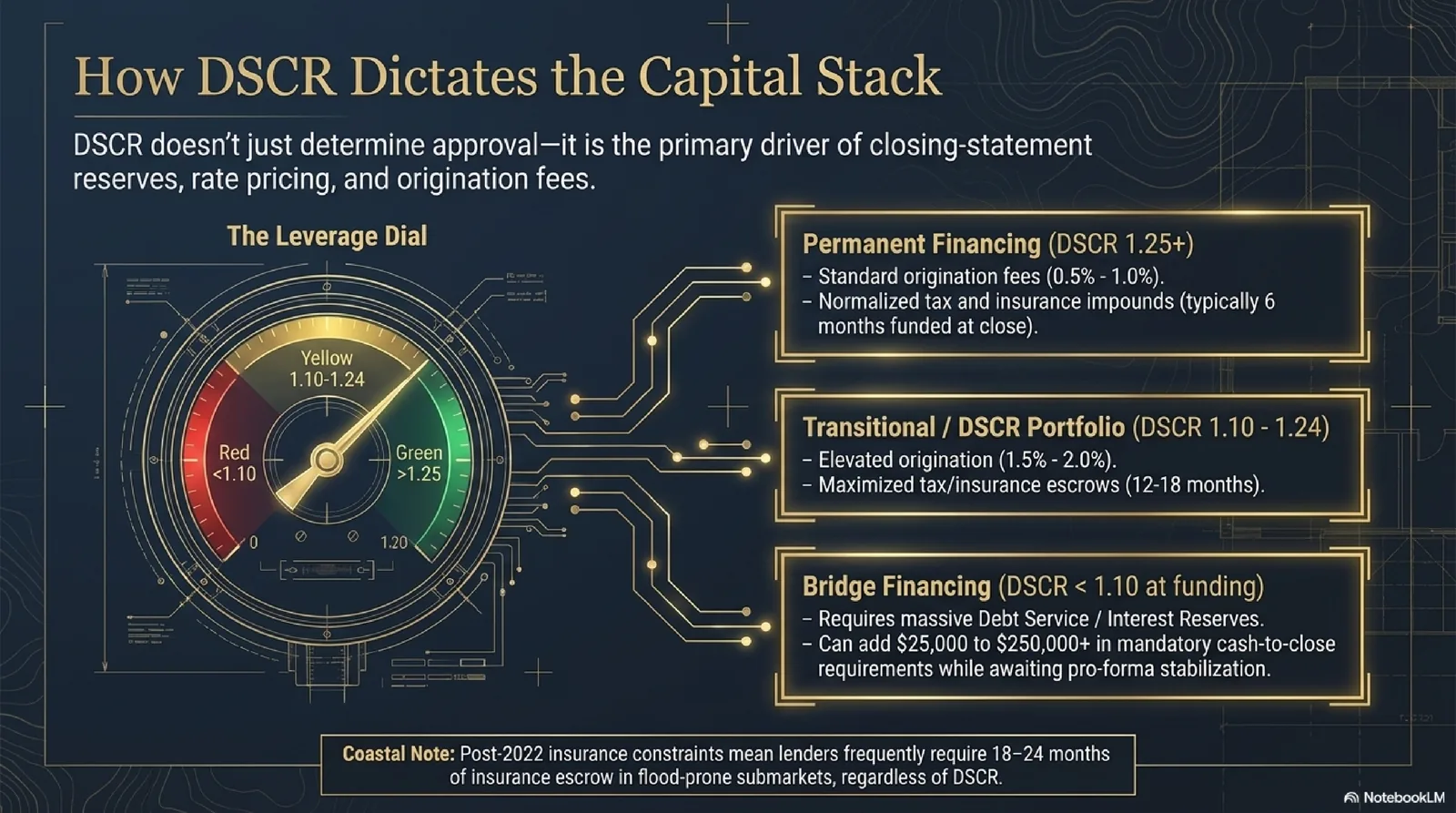

The Debt Service Coverage Ratio (DSCR) is not just an underwriting metric — it is one of the three biggest drivers of a Florida commercial deal's total cash to close. Every Florida lender, from agency multifamily to bridge to community-bank balance-sheet to portfolio DSCR products, sizes loans, prices rate, and structures reserves based on the property's DSCR. Understanding how DSCR moves the closing cost stack is the difference between modeling 4 percent of price and discovering 5.5 percent at the table.

How DSCR affects Florida lender fees, rate, and points

On Florida commercial loans, the relationship between DSCR and pricing is direct and almost linear within program ranges. A deal underwritten at the lender minimum (typically 1.20–1.25 DSCR for permanent financing) generally pays the program's full origination fee and a base rate. Every 0.10 DSCR above the minimum typically buys 5–15 basis points of rate improvement and modest origination-fee relief. Conversely, a deal that comes in 0.05 DSCR below the lender's floor frequently triggers loan downsizing, a pricing bump of 25–50 basis points, or a structured holdback that adds carry and complexity to the closing.

For bridge financing on transitional Florida assets, DSCR sensitivity is even sharper. A bridge lender writing to a 1.00–1.10 in-place DSCR will often require an interest reserve sized to cover 6–24 months of debt service if the pro-forma stabilization plan slips — that reserve is funded at closing and runs anywhere from $25,000 to $250,000+ on Florida bridge deals between $2M and $15M. The reserve sits on the closing statement as cash-to-close, materially changing the equity check the buyer writes.

How DSCR affects reserves and escrows at closing

Florida commercial lenders use DSCR to size three categories of closing-statement reserves: (1) tax and insurance impounds — weaker DSCR deals typically face 12–18 months of property-tax and insurance escrow funded at close, vs 6 months for stronger-DSCR deals (a difference of $25,000–$80,000 on a typical $5M Florida multifamily); (2) debt service or interest reserves — standard on bridge and construction loans, frequently required on permanent loans where DSCR is at or near the floor; and (3) capex and lease-up reserves — common on office and retail acquisitions where the property is below stabilization, typically 6–18 months of operating shortfall funded at closing.

For Florida coastal exposure post-2022 insurance crisis, lenders have begun requiring 18–24 months of insurance escrow on properties in flood-prone or hurricane-exposed submarkets — a structural change that has added $15,000–$50,000 to typical Florida coastal-CRE closings over the past 36 months. Run your DSCR before bidding to anticipate which reserve tier your deal will land in.

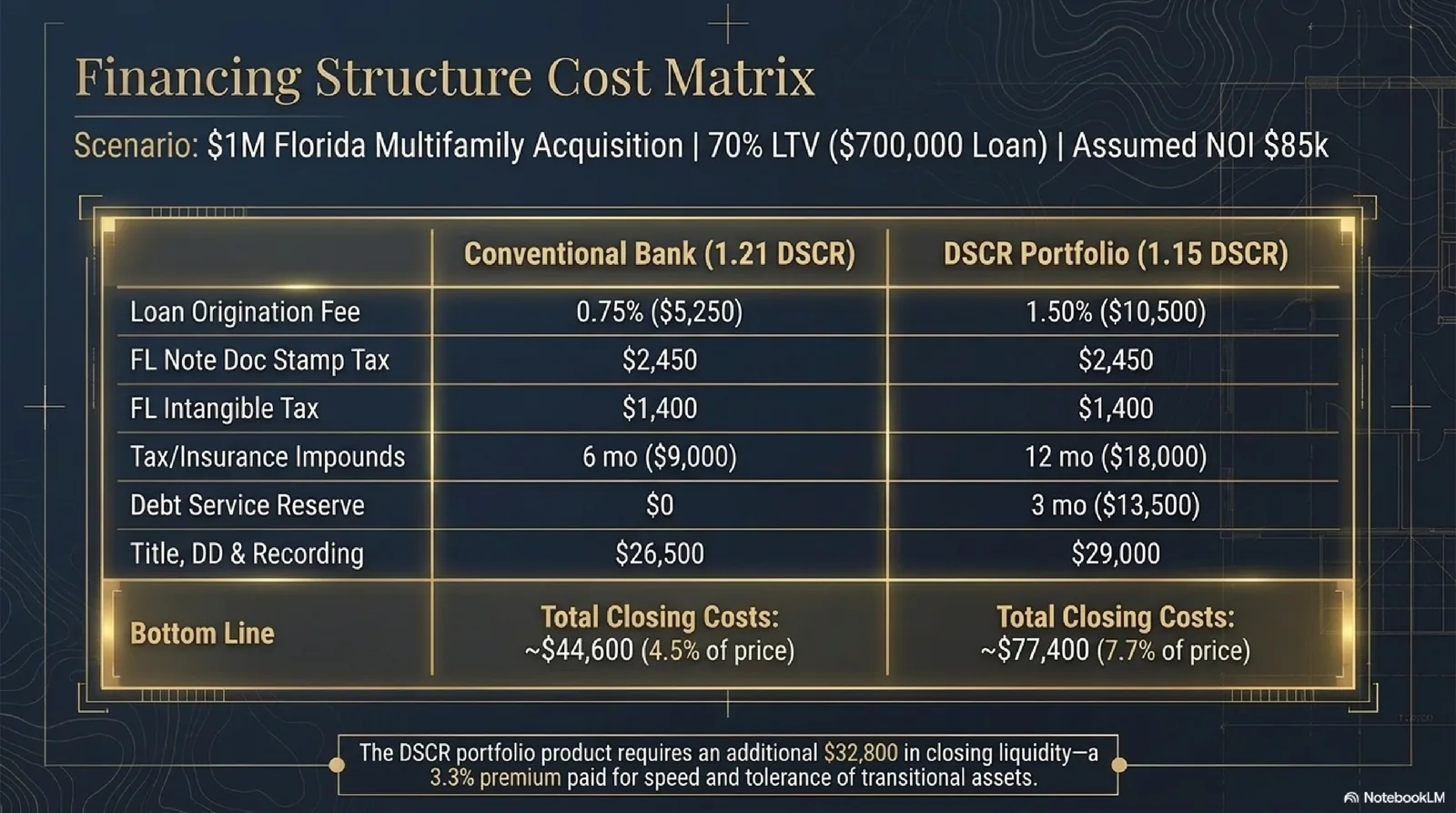

Worked example: $1M Florida CRE deal — conventional bank loan vs DSCR loan

To make the DSCR/closing-cost relationship concrete, here is a side-by-side comparison of the same Florida small-balance commercial acquisition financed two different ways: a conventional community-bank permanent loan vs a portfolio DSCR loan. Property: $1M acquisition, multifamily, Polk County (outside Miami-Dade surtax zone), 70 percent LTV ($700,000 loan), assumed NOI $85,000, modeled 1.21 DSCR on the conventional bank loan and a 1.15 DSCR on the DSCR portfolio loan.

| Closing Cost Line Item | Conventional Bank Loan | DSCR Portfolio Loan |

|---|---|---|

| Origination Fee | 0.75% of loan = $5,250 | 1.50% of loan = $10,500 |

| Florida Doc Stamp Tax on Note (buyer) | 0.35% of loan = $2,450 | 0.35% of loan = $2,450 |

| Florida Nonrecurring Intangible Tax | 0.20% of loan = $1,400 | 0.20% of loan = $1,400 |

| Lender Legal | $3,500 | $5,500 |

| Appraisal (lender-ordered) | $3,500 | $4,500 |

| Phase I ESA | $2,800 | $3,200 |

| ALTA/NSPS Survey | $4,500 | $4,500 |

| Lender Title Policy (simultaneous) | $2,200 | $2,800 |

| Owner's Title Policy | $5,000 | $5,000 |

| Tax/Insurance Impound Reserves | 6 mo = $9,000 | 12 mo = $18,000 |

| Debt Service / Interest Reserve | $0 | 3 mo = $13,500 |

| Lender Underwriting / Processing | $2,500 | $3,500 |

| Settlement / Closing Fee | $2,000 | $2,000 |

| Recording Fees | $500 | $500 |

| Total Closing Costs | ~$44,600 (4.5% of price) | ~$77,400 (7.7% of price) |

| Total Cash to Close (incl. 30% down) | ~$344,600 | ~$377,400 |

The DSCR portfolio loan adds approximately $32,800 of additional closing-side cash on this $1M Florida acquisition — roughly 3.3 percent of purchase price. Whether the premium is worth it depends on whether the deal qualifies for the conventional bank loan in the first place. For non-stabilized assets, recent ownership changes, weaker borrower credit, or properties the bank views as transitional, the DSCR product is often the only viable path — making the higher closing cost stack the price of getting the deal done at all.

Use the DSCR Calculator to instantly model your deal's DSCR and see which loan programs you qualify for, then run the full closing-cost stack in the Florida CRE Closing Cost Calculator. For the complete DSCR formula, lender minimums by program, and how DSCR factors into CREDDS distress detection, read the full DSCR guide for Florida commercial investors.

Stop Guessing Your Closing Costs — Model Them Before You Bid

Linton Global Solutions' interactive Florida CRE Closing Cost Calculator builds a full line-item estimate specific to your deal size, financing structure, and Florida county. Know your real cash-to-close before you submit.

Use the Closing Cost Calculator →FAQ: Florida Commercial Closing Costs

What is the documentary stamp tax rate in Florida for commercial real estate?

Under Florida Statutes Chapter 201, the doc stamp tax on commercial deeds is $0.70 per $100 of the purchase price in all counties except Miami-Dade, where the combined rate is $1.05 per $100 for non-residential properties. A separate doc stamp tax of $0.35 per $100 applies to the mortgage promissory note, and there is no cap on this amount for commercial mortgages secured by Florida real property.

What is the nonrecurring intangible tax on a Florida commercial mortgage?

The nonrecurring intangible tax under Florida Statutes Section 199.133 is 2 mills — $2.00 per $1,000 of the mortgage amount, or 0.2 percent of the loan. There is no cap for commercial mortgages secured by Florida real property, so a $15 million loan generates $30,000 in intangible tax at closing.

Who pays for title insurance on a commercial real estate closing in Florida?

Florida law does not mandate which party pays for title insurance — it is determined by the purchase and sale agreement and local market custom. In most Florida counties including Orange, Osceola, Polk, and Hillsborough, buyer-pays is the prevailing custom, while in some other counties the seller typically pays. On bank REO dispositions, the seller often designates the title company.

How much does an ALTA survey cost for a commercial property in Florida?

ALTA/NSPS surveys in Florida generally run $4,000–$12,000 for standard commercial transactions, with Orlando-area pricing at the lower end for simple properties and complex multi-acre assemblages potentially exceeding $25,000. Rush turnarounds add 25–100 percent on top of base pricing, and lender-required Table A optional items add further cost.

What does a Phase I ESA cost for a Florida commercial property?

Phase I Environmental Site Assessment costs in Florida range from $1,500–$2,500 for low-risk small properties, $2,000–$4,000 for standard commercial assets, and $4,000–$10,000+ for industrial, brownfield, or complex-use sites. Florida-specific concerns including underground storage tanks and dry cleaner contamination can push costs to the high end.

What are total buyer closing costs as a percentage of purchase price for a Florida commercial deal?

Institutional-grade Florida commercial transactions typically generate buyer-side closing costs of 3–5 percent of the purchase price, excluding the down payment — materially higher than the 3.2 percent national average due to Florida's two-layer documentary stamp and intangible tax structure, state-filed title insurance rates, and mandatory commercial due diligence requirements.

What is the typical buyer closing costs percentage for commercial real estate?

The typical buyer closing costs percentage for commercial real estate runs 2.5–4 percent of purchase price nationally and 3–5 percent in Florida specifically. The Florida premium comes from the documentary stamp tax (0.7 percent of price), the nonrecurring intangible tax on the mortgage (0.2 percent of loan amount), and Florida's state-filed title insurance promulgated rates. On a $5 million Florida commercial deal financed at 65 percent LTV, expect roughly $175,000–$240,000 in buyer-side closing costs before any lender-specific fees.

What are typical buyer closing costs for a commercial real estate acquisition?

Typical buyer closing costs in a commercial real estate acquisition include: title insurance (0.4–0.6 percent of price), documentary stamp tax (varies by state — 0.7 percent in Florida), recording and filing fees ($100–$2,500 depending on document count), ALTA survey ($4,000–$12,000), Phase I Environmental Site Assessment ($1,500–$10,000), property appraisal ($3,000–$10,000), legal counsel ($5,000–$50,000+), lender origination fees (0.5–2 percent of loan), and lender-mandated reserves. Total runs 3–5 percent of purchase price for a typical Florida transaction.

What is the standard buyer closing costs percentage for commercial real estate?

The standard buyer closing costs percentage for commercial real estate transactions is 2.5–5 percent of purchase price, depending heavily on state taxes, loan structure, and asset complexity. Cash deals come in at the low end (no lender fees, no intangible tax). Highly leveraged acquisitions with extensive due diligence (Phase II ESA, geotechnical, structural, etc.) come in at the high end. Florida specifically runs 3–5 percent because of state-mandated doc stamps and intangible taxes that don't exist in most other states.

What is the typical buyer closing costs percentage for Florida commercial real estate?

The typical buyer closing costs percentage for Florida commercial real estate is 3–5 percent of purchase price, excluding the down payment. The Florida-specific cost stack includes documentary stamp tax (0.7 percent of price; 1.05 percent for non-residential in Miami-Dade), nonrecurring intangible tax on the mortgage (0.2 percent of loan with no cap), state-filed title insurance rates, ALTA/NSPS surveys, Phase I ESAs (often Phase II in Central and South Florida), and lender fees. A $10M deal financed at 65 percent LTV typically generates $300,000–$500,000 in closing costs.

What is the typical buyer closing costs percentage for commercial warehouse or industrial property?

Industrial and warehouse commercial property closings typically run 3–4.5 percent of purchase price on the buyer side — slightly lower than retail or hospitality assets because the due diligence stack is leaner (no franchise agreements, no liquor licenses, no PIP exposure). However, Florida industrial assets often require a Phase II ESA ($8,000–$25,000) and geotechnical investigation ($5,000–$15,000) if the site has any prior industrial use, pushing total closing costs to the higher end of the range. Heavy-truck-traffic sites near port terminals (PortMiami, Port Everglades, Port Tampa Bay, JAXPORT) carry additional environmental scrutiny.

What is the typical acquisition closing costs percentage for commercial real estate?

The typical acquisition closing costs percentage for commercial real estate is 2.5–5 percent of total purchase price. The buyer side carries the majority of this stack: title, doc stamps, intangible tax (in Florida), survey, ESA, appraisal, legal, lender origination, and impound reserves. Seller-side costs are smaller — typically 0.5–2 percent — and primarily consist of broker commissions (paid by seller in most Florida deals), seller legal fees, and any agreed-upon doc stamp share. The 3.2 percent national average understates Florida transactions by 30–60 basis points.

What are typical commercial loan closing costs?

Typical commercial loan closing costs include: origination fee (0.5–2 percent of loan amount, lender-dependent), lender legal fees ($3,000–$25,000), appraisal ordered by lender ($3,000–$10,000), Phase I ESA ordered by lender ($1,500–$10,000), title insurance lender's policy (50–60 percent of owner's policy rate), survey if not provided by buyer ($4,000–$12,000), recording and intangible tax on the mortgage (0.2 percent of loan in Florida), and lender impound reserves for taxes, insurance, and CapEx ($25,000–$250,000+ depending on asset size). On a $6.5M commercial loan in Florida, total loan-side closing costs typically run $90,000–$180,000.

How much should a buyer budget for closing costs on a commercial real estate deal in Florida?

Conservative buyer budgeting rule for Florida commercial real estate: 4 percent of purchase price for institutional-grade transactions, plus an additional 0.5–1 percent buffer for surprises (deferred maintenance discovered in inspection, environmental issues uncovered in Phase I/II, title curative work, lender-required reserves). On a $3M deal, budget $135,000–$165,000. On a $10M deal, budget $400,000–$500,000. The actual outcome depends heavily on loan structure and asset due diligence complexity — cash deals on simple assets can close at 1.5–2.5 percent total.

What closing costs are commonly missed when underwriting a Florida commercial real estate deal?

The most commonly underestimated Florida CRE closing costs are: (1) the nonrecurring intangible tax on the mortgage — uncapped, 0.2 percent of loan, often forgotten until the closing statement; (2) hurricane and flood insurance premium bind-up for the first year — Florida insurance rates have spiked 30–80 percent post-2022; (3) Phase II ESA when Phase I flags a recognized environmental condition (REC) — typical Phase II runs $8,000–$25,000; (4) lender-mandated impound reserves for taxes and insurance that can equal 12–18 months of escrow funded at close; (5) Miami-Dade County's 1.05-percent doc stamp surcharge on non-residential property; and (6) the cost of curing a chain-of-title defect (typical $2,000–$15,000 in legal work).

What is DSCR and why does it matter for Florida commercial loans?

DSCR (Debt Service Coverage Ratio) is the ratio of a property's Net Operating Income (NOI) to its annual debt service. DSCR = NOI ÷ Annual Debt Service. On a Florida commercial loan, DSCR drives three things directly: (1) the maximum loan amount the lender will offer — most Florida CRE lenders size loans backwards from a 1.20–1.25 DSCR floor; (2) the interest rate and points charged — every 0.10 DSCR above the lender minimum typically buys 5–15 basis points of rate improvement; and (3) the size of impound reserves required at closing — weaker DSCR deals frequently trigger interest reserves, debt service reserves, or capex holdbacks of $25,000–$250,000+. For Florida bridge and DSCR loans specifically, the property must demonstrate adequate DSCR even when the borrower's personal income is excluded — making DSCR the single most important underwriting metric on Florida investment-property financing. See our full DSCR guide for the formula, lender minimums by program, and Florida-specific examples.

What are typical closing costs for a DSCR loan on a Florida commercial property?

DSCR loan closing costs on Florida commercial property typically run 4–6 percent of the loan amount — slightly higher than conventional bank financing because DSCR loan products (often portfolio or private-label paper) carry higher origination fees, additional underwriting touchpoints, and richer reserve requirements. Typical line items on a $1M Florida DSCR loan: origination fee 1.0–2.0 percent ($10,000–$20,000), Florida nonrecurring intangible tax 0.2 percent of loan ($2,000), documentary stamp tax on note 0.35 percent ($3,500), lender legal $3,000–$8,000, third-party reports (appraisal, ESA, survey) $7,500–$22,000 ordered by lender, lender impound reserves $15,000–$60,000 (6–12 months tax/insurance escrow), and lender title policy $3,000–$6,000 (simultaneous issue discount). Combined DSCR loan closing cost stack: roughly $44,000–$120,000 on a $1M Florida deal, vs $30,000–$75,000 on a comparable conventional bank loan.

How do DSCR requirements change between Florida bridge loans and permanent financing?

DSCR thresholds widen significantly between Florida bridge and permanent financing because the two product types are designed for different points in the asset life cycle. Florida bridge loans typically require a minimum DSCR of 1.00–1.10 at funding, with the lender underwriting to a pro-forma stabilized DSCR of 1.25–1.40 within 18–36 months — the bridge lender is financing a transitional asset where current NOI is depressed but a clear stabilization plan exists. Permanent financing (CMBS conduit, agency multifamily, life-company, or bank balance-sheet) requires DSCR at funding: agency Fannie/Freddie multifamily at 1.25, CMBS at 1.20–1.25, HUD 223(f) refi at 1.11 (lowest in the industry), SBA 504 at 1.15–1.25, and hotel CMBS at 1.40+. For Florida-specific deal modeling, build the bridge-to-perm DSCR escalation into your underwriting before you bid — most failed Florida bridge takeouts are caused by a stabilization plan that delivers a stabilized DSCR below the permanent lender's floor.

What DSCR do lenders usually require on Florida investment properties?

For Florida investment-property financing, the prevailing DSCR minimums by program are: agency multifamily (Fannie Mae DUS, Freddie Mac SBL) at 1.25; CMBS conduit at 1.20–1.25 for office/retail/industrial and 1.40+ for hotel; bank balance-sheet permanent at 1.25–1.30 (community and regional banks); life-company permanent at 1.30–1.40 (favoring stabilized core assets); HUD multifamily 223(f) at 1.11; SBA 504 owner-occupied at 1.15–1.25; DSCR loan products (non-QM portfolio paper) at 1.00–1.20 depending on credit overlays; and Florida bridge financing at 1.00–1.10 at funding with a stabilization plan to 1.25+. Florida-specific lender preferences: top-tier I-4 corridor markets (Orlando, Tampa, Lakeland) earn modest DSCR relief on multifamily and industrial; coastal hurricane-exposed assets (especially post-2022 insurance crisis) often see DSCR floors tighten by 0.10–0.15; and small-balance bank lenders in Florida have meaningfully tightened DSCR requirements through 2025–2026 in response to CRE stress.

How can investors lower DSCR loan closing costs on a Florida commercial deal?

Five concrete levers to lower DSCR loan closing costs on a Florida commercial deal: (1) Negotiate origination fee — on $1M+ DSCR loans, originators routinely cut origination from 2.0 percent to 1.0–1.25 percent if the borrower has clean credit, prior performance, and runway to close in 30 days; (2) Cap the third-party report spend — get lender-approved appraiser and ESA firms, push back on Table A survey items that aren't lender-mandated, and reuse a Phase I from a recent prior owner if within ASTM E1527-21 update windows; (3) Negotiate impound reserves down — strong-DSCR deals (1.30+) frequently win 6-month rather than 12-month tax/insurance escrow; (4) Use simultaneous-issue title insurance — the lender's policy at simultaneous issue can be 50–70 percent cheaper than a standalone issue; and (5) Time the close around Florida's November–February property-tax discount window (4 percent off in November, declining to 1 percent by February) — a $100,000+ annual tax bill captures real dollars from this single timing decision. Model the full stack with our Florida Closing Cost Calculator before you bid.

What DSCR do you need for a commercial loan in Florida?

Most Florida commercial lenders require a minimum DSCR of 1.20–1.25 at funding for permanent financing, with bridge and DSCR-loan products accepting as low as 1.00–1.10 with appropriate compensating factors. The practical answer depends on three variables: loan program (Fannie/Freddie agency 1.25, CMBS 1.20–1.25, HUD 1.11, SBA 1.15–1.25, bank permanent 1.25–1.30, hotel CMBS 1.40+, bridge 1.00–1.10); asset class (multifamily and industrial enjoy the tightest DSCR; office and retail face stress in 2025–2026; hospitality requires the highest); and market/insurance exposure (Florida coastal assets post-2022 insurance crisis frequently face DSCR floor adjustments of +0.10–0.15). For pre-bid underwriting, target your pro-forma DSCR at 0.10 above the lender minimum to absorb rate moves, NOI variance, and insurance shocks during the pricing period.

Are DSCR loan closing costs higher than bank loan closing costs in Florida?

Yes — Florida DSCR loan closing costs typically run 50–80 percent higher than comparable bank loan closing costs, primarily because DSCR loan products carry higher origination (1.0–2.0 percent vs 0.5–1.0 percent on bank paper), often include yield-spread premiums or rebates priced into the loan, and frequently require richer reserves (12 months tax/insurance vs 6 months). On a $1M Florida commercial loan, the comparison typically lands at: conventional bank loan total closing costs $30,000–$75,000 (3.0–7.5 percent of loan); DSCR portfolio loan total closing costs $44,000–$120,000 (4.4–12.0 percent of loan). The DSCR loan premium is the cost of speed, lighter borrower documentation, and tolerance for transitional or non-stabilized assets — three things conventional bank financing in Florida's current credit environment will rarely accommodate. Whether the premium is worth it depends on whether the deal qualifies for bank financing at all; for most Florida investor purchases of non-stabilized assets in 2025–2026, DSCR product is the only viable path.

After 39 years closing deals across this state, the single most common reason I see otherwise good deals go sideways at the table is that the buyer modeled three percent closing costs and the real number came in at five percent. In Florida, documentary stamps, intangible tax, and title alone will get you to three percent on most commercial deals before you add a single dollar of survey, environmental, appraisal, or lender fees.

Run the real numbers — use the calculator, model the stack, and size your equity accordingly. The deals that actually pencil are the ones that were underwritten correctly from day one, not the ones that were rescued by a spreadsheet adjustment a week before closing.