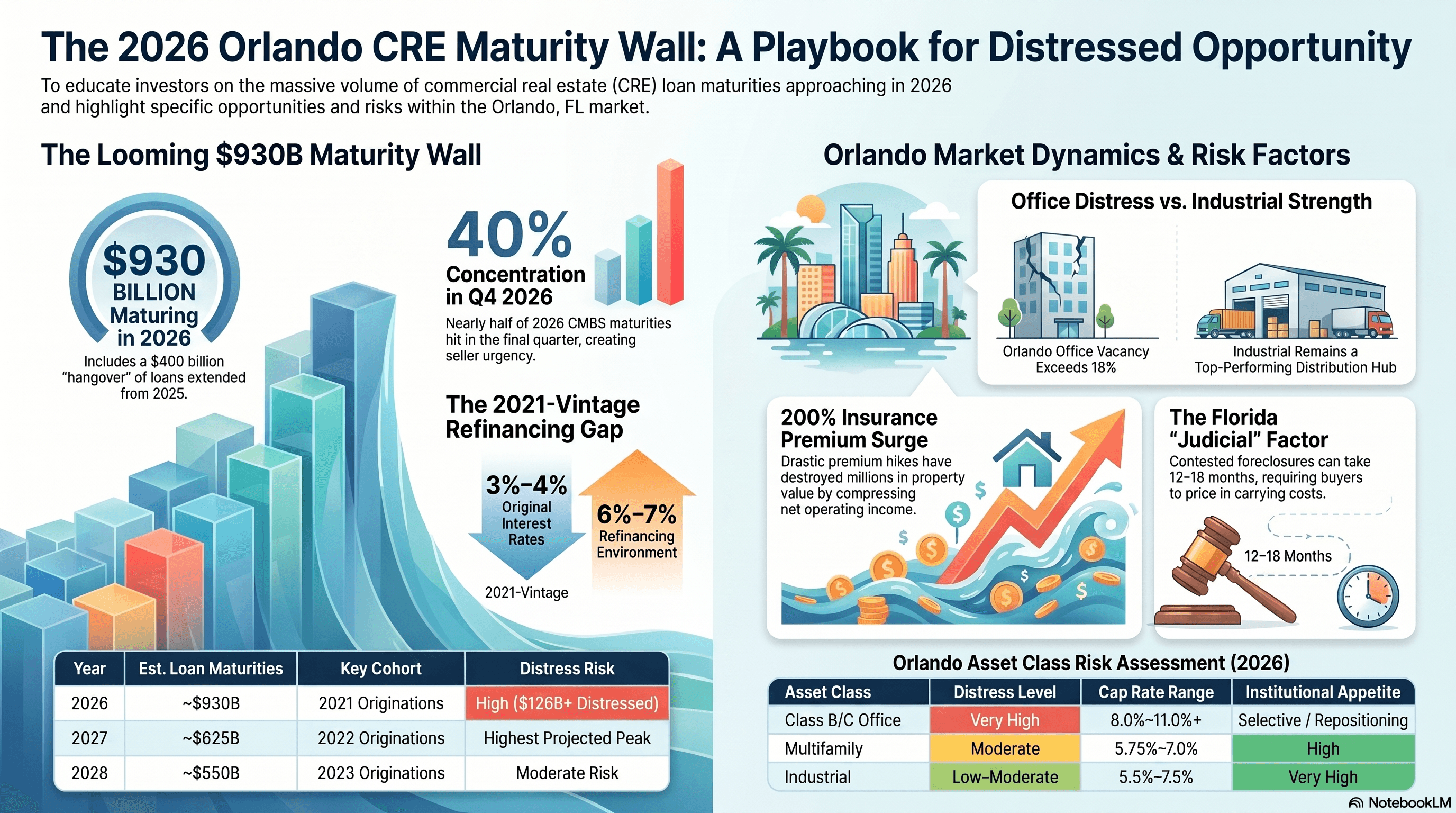

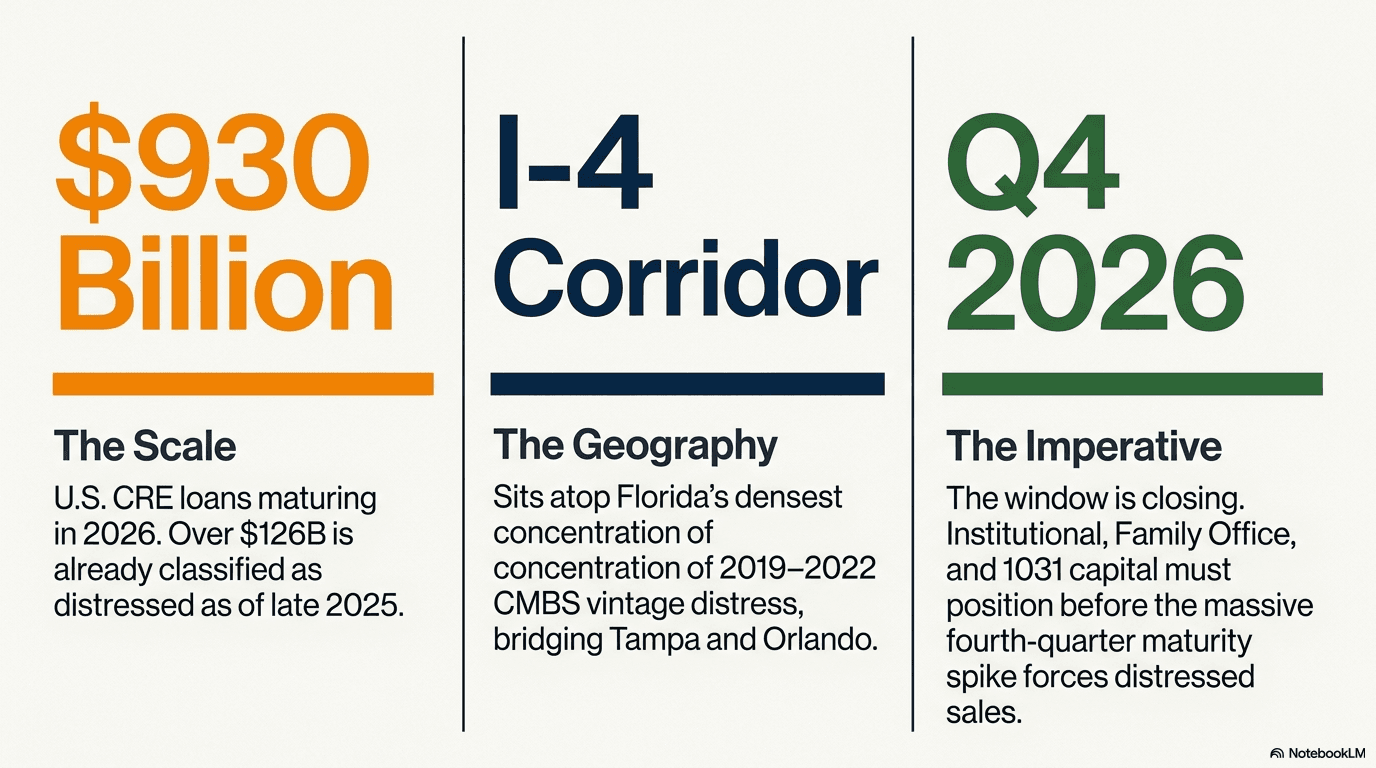

Approximately $930 billion in U.S. commercial real estate loans mature in 2026, with at least $126 billionalready classified as distressed. Orlando's I-4 corridor sits on top of one of the densest concentrations of 2021-vintage CMBS in the country. This piece breaks down where the distress is by asset class, how Florida's judicial-foreclosure and doc-stamp regime shapes acquisition math, how institutional capital is structuring NPL and REO buys, and where 1031 and family-office capital has a structural edge.

The Numbers Nobody Wants to Admit

The commercial real estate industry has spent two years hoping the maturity wall would somehow dissolve on its own. It hasn't. Approximately $930 billion in commercial real estate loans are maturing in 2026 — up significantly from 2025 — and at least $126 billion of that amount was already classified as distressed as of late 2025. The scale here is not theoretical.

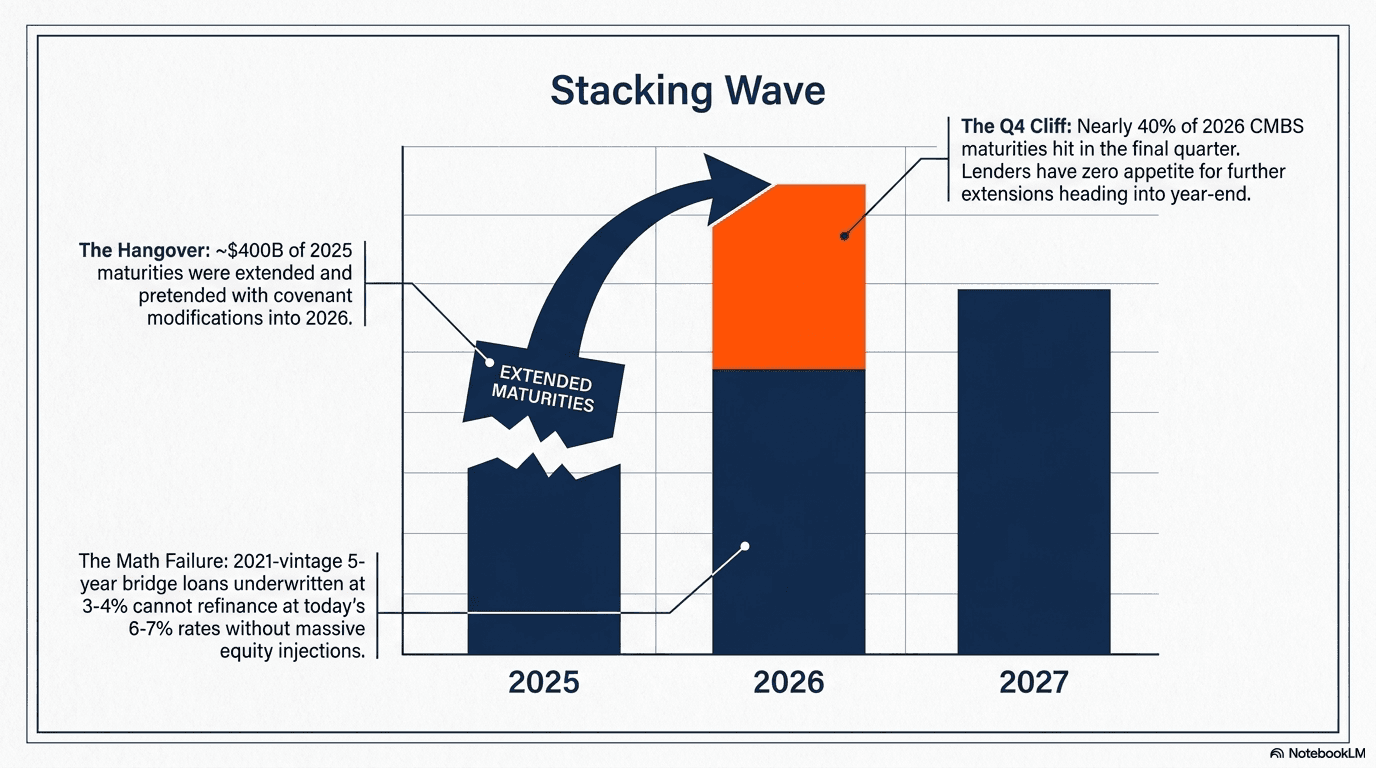

Nearly $400 billion in loans that were supposed to mature in 2025 were extended — often with waiver fees and covenant modifications — into 2026. That means 2026 is carrying its own origination-driven load plus the hangover from a year of extend-and-pretend. MSCI estimates roughly $1.15 trillion in loans are effectively coming due right now when you factor in those rollovers. 2027 then peaks higher still, with approximately $625 billion in fresh maturities stacking on top of whatever 2026 cannot resolve.

For Orlando investors and operators, these are not abstract Wall Street problems. They are the reason three office properties in the Maitland submarket are sitting on servicer watchlists right now. They are the reason community banks along the I-4 corridor are quietly shopping workout packages. The maturity wall is arriving here — and the capital is already following it.

Why Orlando Is Ground Zero for Distressed Opportunity

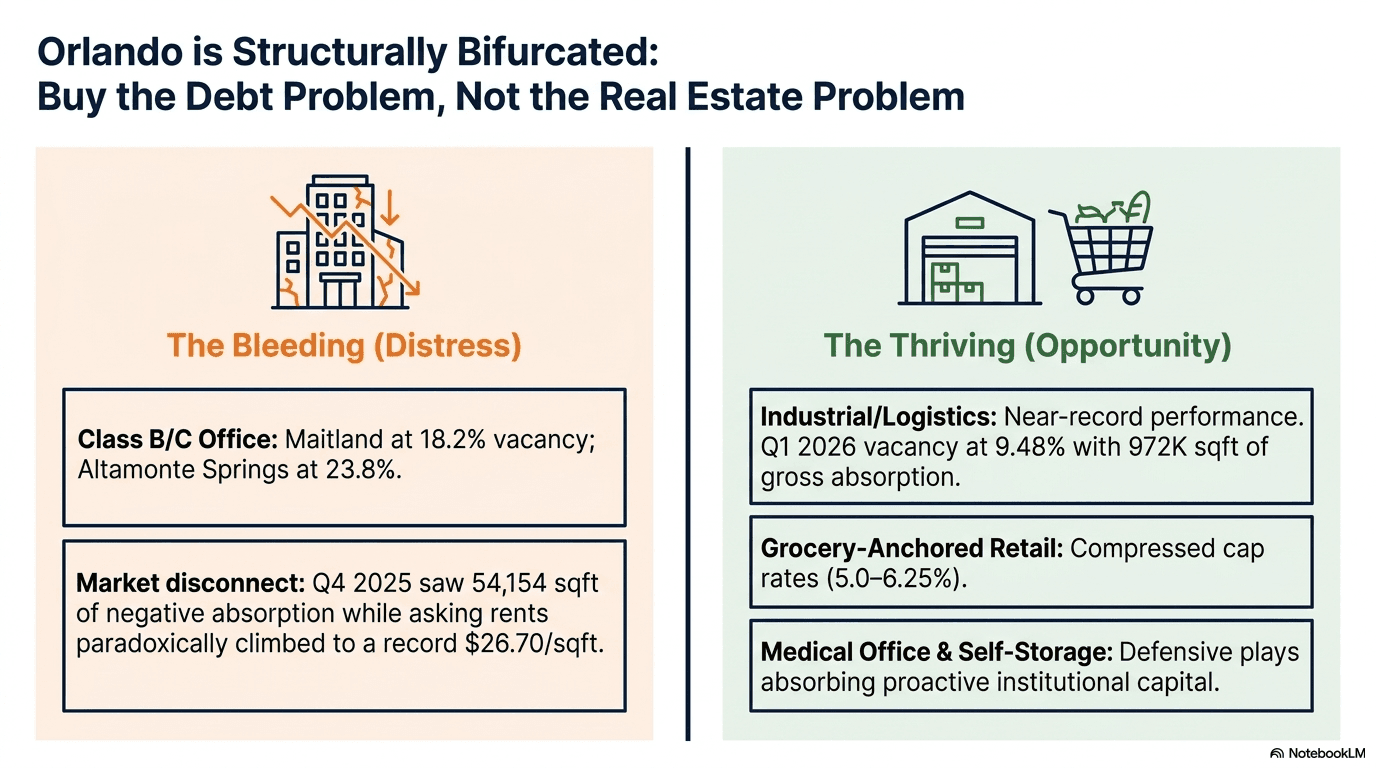

Orlando's CRE market is structurally bifurcated in a way that creates outsized opportunity for prepared buyers. The city's industrial and logistics sector is performing at near-record levels — Central Florida industrial vacancy stood at 9.48% in Q1 2026, rising modestly only due to 1.4 million square feet of new deliveries, while gross absorption remained strong at nearly 972,000 square feet. Tenant demand is real and active.

The office picture is the opposite. Maitland's office vacancy stood at 18.2% and Altamonte Springs hit 23.8% as of Q1 2025 data — well above the national office vacancy of 18.6%. The Orlando market overall posted 54,154 square feet of negative absorption in Q4 2025, even as asking rents paradoxically climbed to a record $26.70 per square foot. That disconnect — rising ask, falling occupancy — is a classic leading indicator of distressed loan pressure building beneath the surface.

The I-4 corridor between Orlando and Tampa represents Florida's densest concentration of CMBS-financed commercial assets originated in 2019–2022. Those five-year loans are hitting their refi windows now, in an environment where borrowing costs are 6–7% — against original underwriting at 3–4%. The math doesn't work for a significant percentage of these properties, and that is where the opportunity lives.

Decoding the Maturity Wall: What Matures, and When

Not all of the maturity wall is distressed — but a disproportionate share is. Morningstar DBRS has projected that more than half of the $100+ billion in fixed- and floating-rate CMBS loans coming due in 2026 will not repay at maturity. That is an extraordinary statement from a credit rating agency, and it has direct implications for Florida assets backing those loans.

The vintage concentration is important. The bulk of near-term maturities traces to 2021 originations — particularly five-year multifamily and office bridge loans that were underwritten assuming continued rent growth and stable cap rates. Cap rates have since expanded by 150–200 basis points across most Central Florida asset classes, meaning refinancing today requires either a significant paydown or a new equity partner willing to accept the current basis.

CRE Maturity Wall — National Volume by Year and Distress Concentration

| Year | Est. Loan Maturities | Key Cohort | Distress / Refi Risk |

|---|---|---|---|

| 2025 (extended) | ~$400B rolled into 2026 | 2020 bridge originations | High — already on extension |

| 2026 | ~$930B scheduled | 2021 originations (5-yr) | High — $126B+ distressed |

| 2027 | ~$625B peak | 2022 originations (5-yr) | Highest projected year |

| 2028 | ~$550B | 2023 originations (mixed) | Moderate — depends on rates |

Sources: ForvisMazars, MSCI Real Capital Analytics, S&P Global Market Intelligence, Morningstar DBRS.

The Q4 2026 maturity concentration deserves special attention. Nearly 40% of 2026 CMBS maturities are scheduled in the final quarter — meaning borrowers and servicers face a compressed window to resolve or restructure, and lenders have limited appetite for more extend-and-pretend heading into year-end. That calendar pressure is a catalyst for motivated selling.

Florida's Legal and Cost Architecture — What Institutional Buyers Must Price In

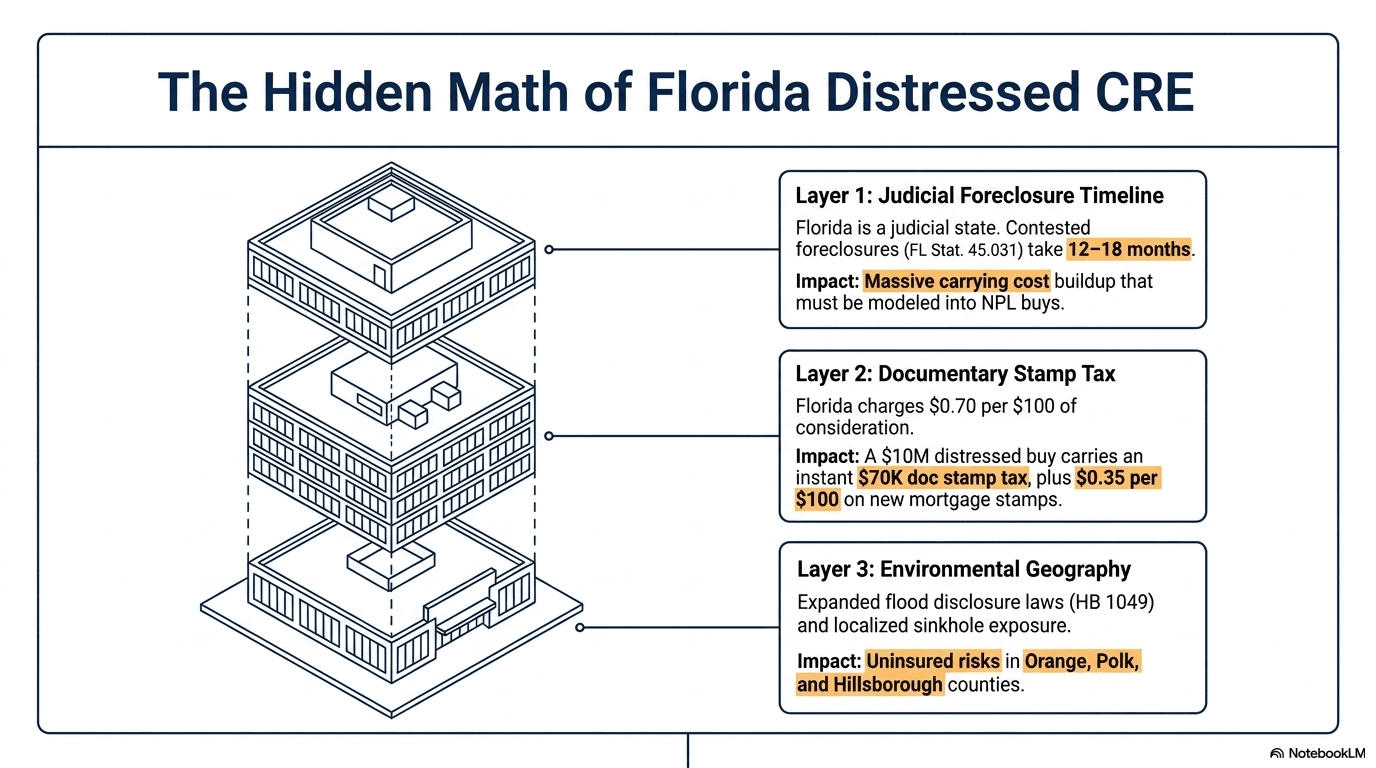

Florida's judicial foreclosure framework is the first thing any out-of-state institutional buyer needs to understand before underwriting a distressed acquisition here. Unlike non-judicial states where a lender can foreclose through a trustee sale in as little as 90 days, Florida requires the lender to file a civil lawsuit, obtain a final judgment, and then schedule a public sale — a process governed by Florida Statutes Section 45.031. A hotly contested foreclosure can exceed 12–18 months from default notice to gavel. That timeline is a carrying cost that must be built into every NPL or REO pricing model.

Documentary stamp tax is a second transaction cost that catches unsophisticated buyers flat-footed. Florida imposes $0.70 per $100 of consideration on deed transfers in all counties except Miami-Dade — meaning a $10 million distressed acquisition carries $70,000 in doc stamps alone, due at recording. Mortgage document stamps add $0.35 per $100 of indebtedness on new financing. For a leveraged acquisition, that adds up fast. Competent deal structuring — including the use of deed-in-lieu transactions and careful analysis of whether a transfer-in-lieu of foreclosure triggers doc stamps on the discharged debt — can meaningfully change the economics.

Florida's flood zone and sinkhole exposure creates a third layer of due diligence that national buyers routinely underestimate. Central Florida, despite not being coastal, carries real sinkhole risk — particularly in Orange, Polk, and Hillsborough counties — and standard commercial property policies do not cover sinkhole damage unless specifically endorsed. As of the October 2024 flood disclosure law (HB 1049, codified as Florida Statutes Section 689.302), flood history disclosure obligations have expanded. Insurance premiums on commercial properties have surged over 200% at renewal for some assets — a figure that directly compresses NOI and can turn a marginally cash-flowing property into a genuinely distressed one overnight.

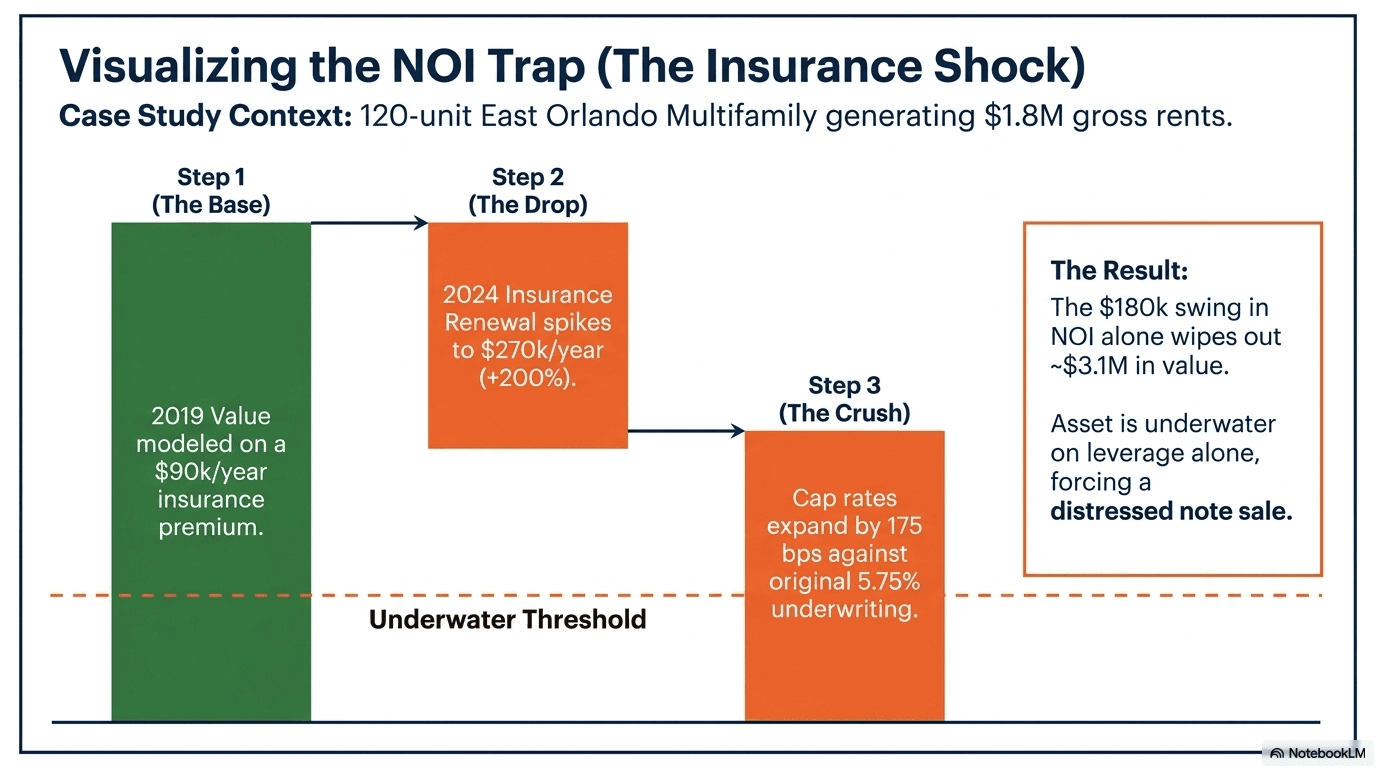

A 120-unit multifamily property in East Orlando generating $1.8M in gross rents carried a $90,000 annual insurance premium in 2019. At 2024 renewal, that same policy came in at $270,000 — a $180,000 annual increase. At a 5.75% cap rate, that swing in NOI alone destroys approximately $3.1 million in value. Buyers who underwrote this asset in 2021 using 2019 insurance comps are now underwater on leverage alone, before accounting for the 175-basis-point cap rate expansion. This is not hypothetical — it describes a real pattern across dozens of I-4 corridor assets.

A Phase I ESA is non-negotiable on every distressed acquisition in Florida. Costs run $2,000–$5,000 for standard commercial parcels in 2026, but industrial or historically contaminated sites can reach $10,000 or more before Phase II sampling. The ASTM E1527-21 standard applies, and buyers need to ensure their environmental professional is operating within the 180-day component clock to avoid having to refresh interviews and records searches at closing.

Asset Class Breakdown: Where the Distress Is (and Isn't)

Understanding where the distress is concentrated — rather than treating CRE as a monolith — is the difference between disciplined acquisition and expensive mistakes. Florida's market is producing distress unevenly across asset types, and institutional capital is already sorting accordingly.

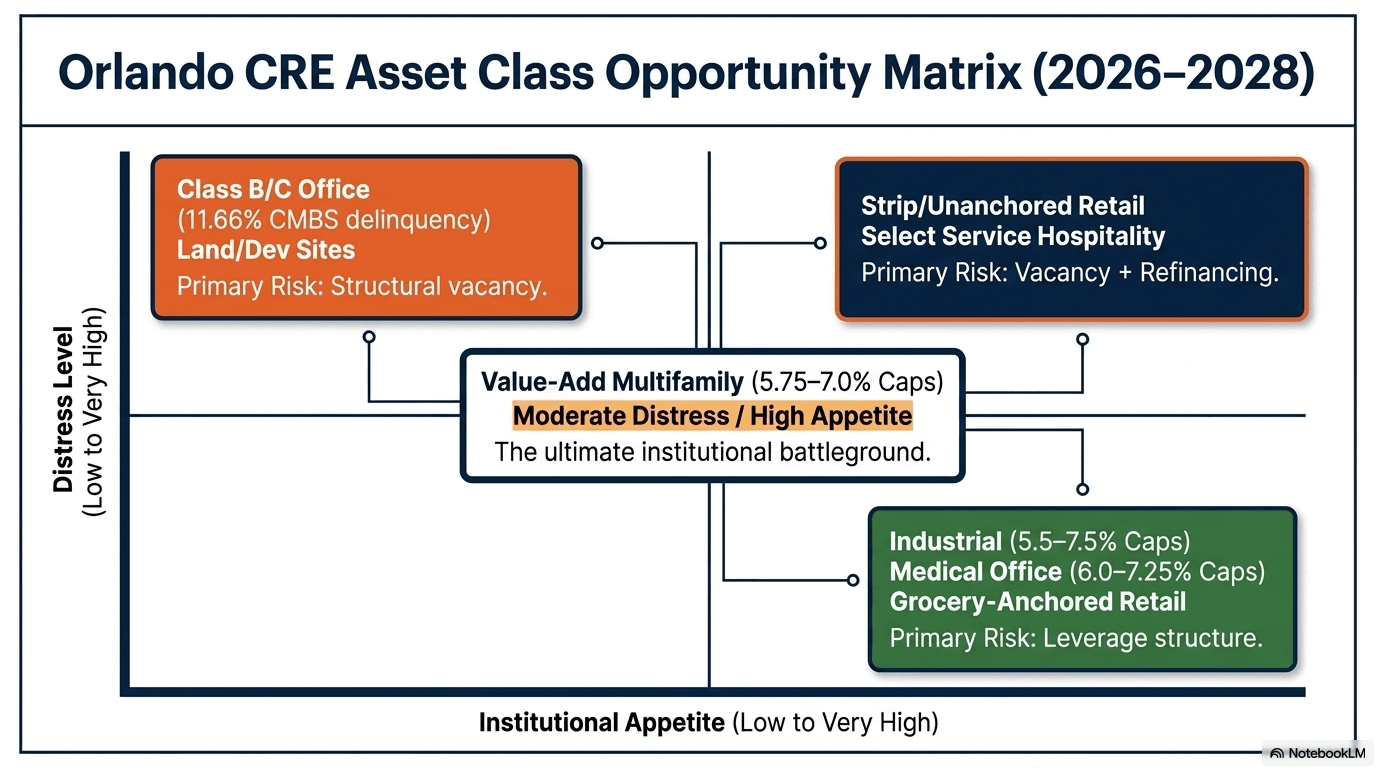

Office carries the deepest structural impairment. The CMBS delinquency rate for office hit 11.66% nationally in August 2025 — the worst-ever recorded level, exceeding even the Global Financial Crisis peak. In Orlando's suburban markets, where legacy Class B product competes against new Class A for a shrinking tenant pool, assets are being repriced 30–50% below their 2021 peak values. Adaptive reuse to medical office or residential is the most common institutional exit thesis, but zoning, floor plates, and HVAC configurations limit that option to a fraction of the inventory.

Industrial and logistics is structurally sound in Central Florida. Orlando leads the state in industrial rent growth, driven by its position as the distribution hub for one of the fastest-growing MSAs in the country. The distress here is idiosyncratic — overleveraged assets with near-term maturities, not fundamental demand problems. That creates clean acquisition opportunities: buy the debt structure problem, not the real estate problem.

Multifamily sits in the middle. Deliveries were substantial in 2024–2025, pushing vacancy up and compressing rent growth. The 2026 forecast is for continued low rental growth, not collapse — but the 2021-vintage bridge loans underwritten at sub-4% rates are now refinancing into a 6–7% environment. For properties with strong occupancy, a discounted bridge loan purchase or preferred equity infusion may be the right structure. For distressed assets with occupancy below 85%, direct REO acquisition is more appropriate.

Retail remains the most bifurcated story. Grocery-anchored and necessity-based retail in the Orlando MSA is performing exceptionally — cap rates on investment-grade NNN product remain compressed at 5.0–6.25%. Strip centers with vacancy above 20%, unanchored product near struggling corridors, and tertiary retail dependent on tourism traffic are the problem assets. Hospitality-adjacent retail along International Drive and US-192 carries particular refinancing risk.

Self-storage and medical office are where institutional capital is moving proactively — not reactively. Self-storage in the I-4 corridor benefits from Orlando's chronic housing undersupply and population transience. Medical office tied to strong healthcare systems is generating below-market financing and near-zero vacancy. These are not distress plays; they are defensive repositioning plays while the office and retail storm works through the system.

Orlando-Area CRE Asset Class Outlook — Distress vs. Opportunity Matrix (2026–2028)

| Asset Class | Distress Level | Cap Rate Range (Orlando) | Institutional Appetite | Primary Risk |

|---|---|---|---|---|

| Class B/C Office | Very High | 8.0%–11.0%+ | Selective / Repositioning | Structural vacancy |

| Class A Office (CBD) | Moderate | 7.0%–8.5% | Active / Opportunistic | Lease rollover risk |

| Multifamily (Value-Add) | Moderate | 5.75%–7.0% | High | Refi cost / Insurance |

| Industrial / Logistics | Low–Moderate | 5.5%–7.5% | Very High | Leverage structure |

| Grocery-Anchored Retail | Low | 5.0%–6.25% | High | Anchor co-tenancy |

| Strip / Unanchored Retail | High | 7.0%–9.5% | Selective | Vacancy + Refi |

| Hospitality (Select Service) | Moderate–High | 7.5%–10.0%+ | Opportunistic | Insurance / Rates |

| Medical Office | Low | 6.0%–7.25% | Very High | Limited supply |

| Self-Storage | Low | 6.0%–7.5% | High | Oversupply risk |

| Land / Development Sites | Very High | Yield on cost | Selective | Entitlement risk |

Cap rates reflect mid-2026 market conditions for stabilized Central Florida assets. Distressed acquisitions target 150–300 bps above stabilized range.

How Institutional Capital Is Structuring the Buys

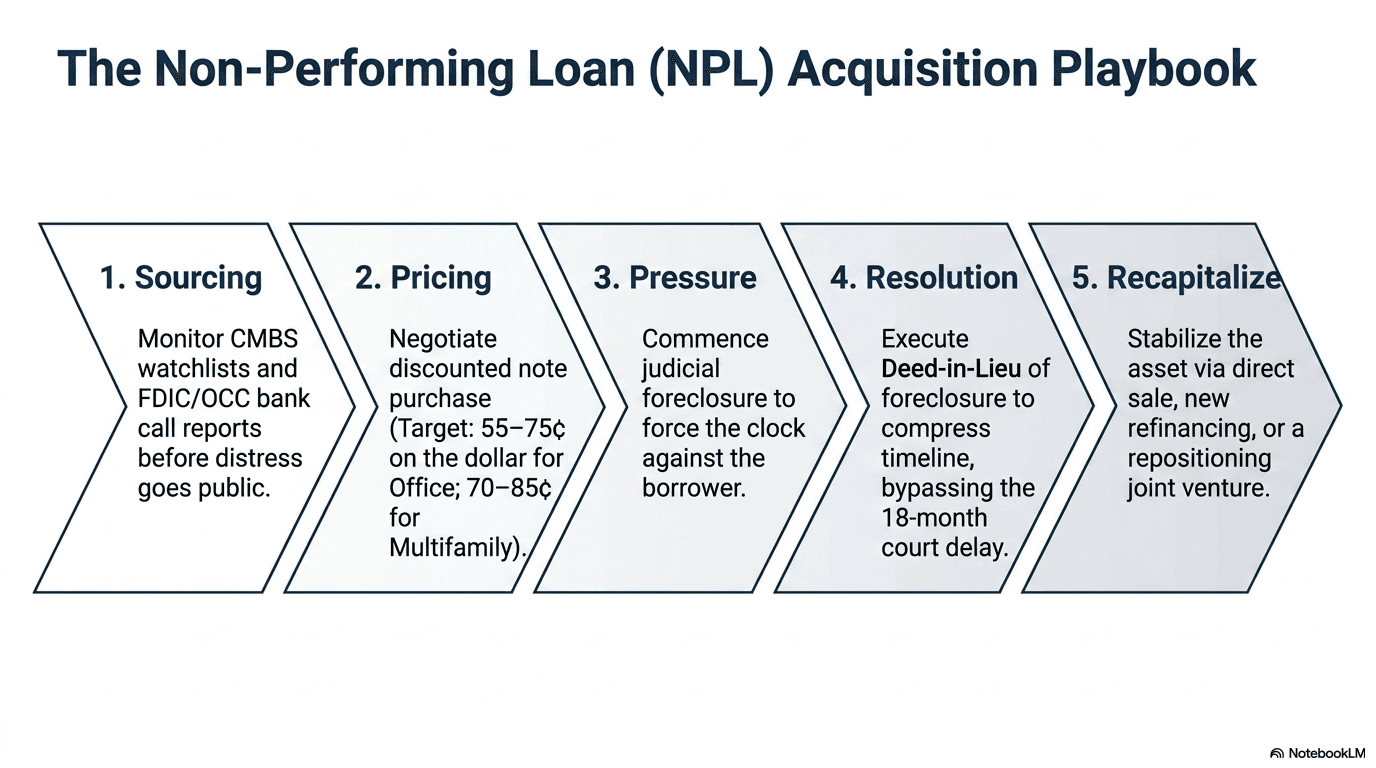

Institutional buyers — private equity funds, family offices, debt funds, and REITs — are not waiting for properties to hit the open market. The most sophisticated operators are acquiring loan positions directly from community banks and CMBS special servicers, then executing either loan workout strategies or foreclosure to obtain the asset at a basis well below replacement cost.

The NPL acquisition playbook in Florida typically follows this sequence: First, identify the distressed loan through servicer watchlist monitoring, FDIC call report analysis, or direct bank relationships. Second, negotiate a discounted purchase of the note — typically 55–75 cents on the dollar for Class B office, 70–85 cents for multifamily depending on occupancy. Third, deliver a payoff letter or commence judicial foreclosure while simultaneously negotiating a deed-in-lieu to compress the timeline. Finally, stabilize and recapitalize through a sale, refinance, or repositioning JV.

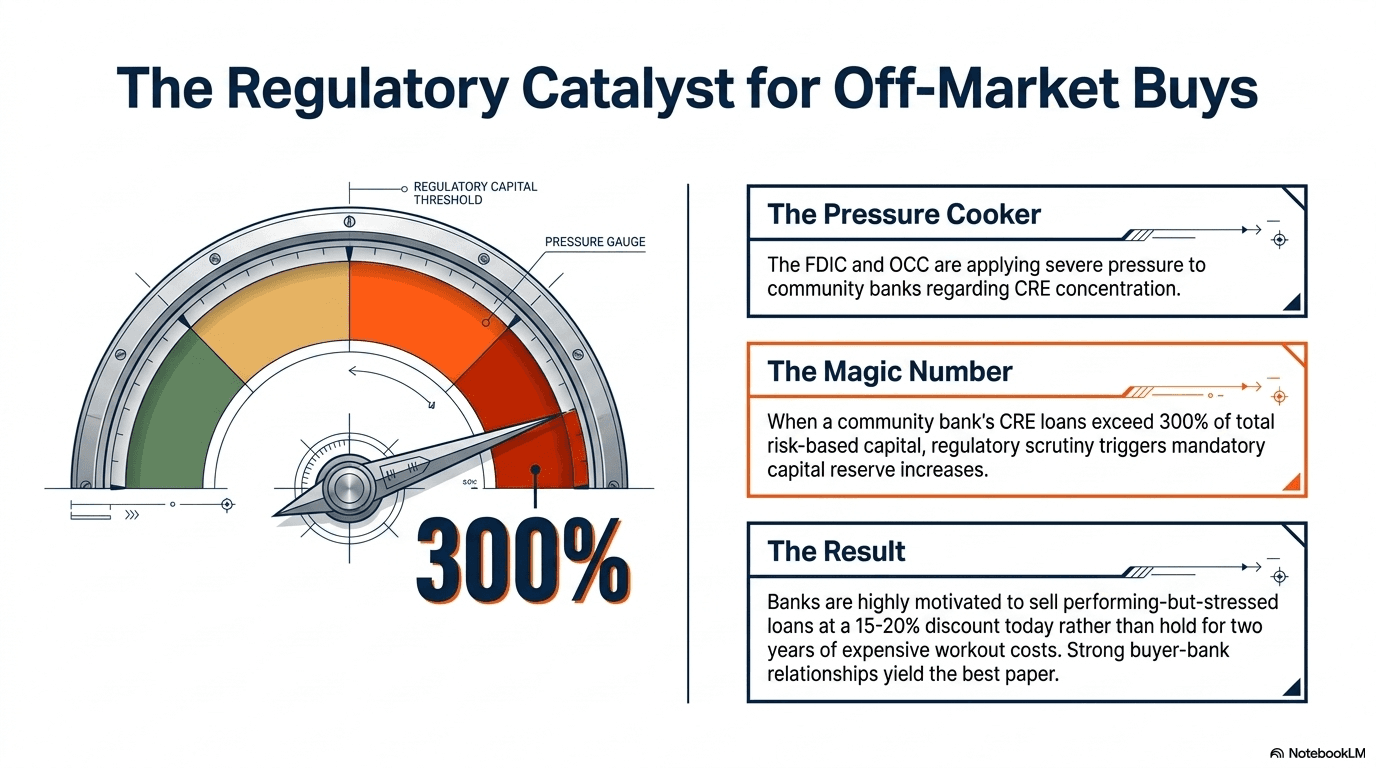

The DSCR math underpins every decision. A property with a 1.05x DSCR at origination may now carry a 0.78x DSCR after insurance escalation, rent softening, and a 200-basis-point rate increase on a floating-rate bridge loan. That coverage gap is where lender motivation to sell the note — rather than carry it — becomes acute. For a community bank facing OCC guidance on CRE concentration limits, the calculus often tips toward a note sale at a modest discount versus holding for two more years of workout costs.

The FDIC has formally advised insured depositories with significant CRE concentrations to maintain elevated capital reserves, bolster loan workout infrastructure, and maintain updated financial analytics on every distressed credit. For community banks where CRE loans exceed 300% of total risk-based capital — a threshold the OCC monitors closely — the pressure to reduce concentration by selling performing-but-stressed loans is real. The 2026 maturity wave is accelerating those conversations at dozens of Florida community banks. Buyers who have established relationships with bank credit officers before assets become overtly distressed will access the best paper at the best pricing.

1031 exchange buyers occupy a different but equally important role in this ecosystem. A cash-out sale of a performing asset creates exchange proceeds that must be deployed within 45 identification and 180 replacement day windows under IRC Section 1031. For a buyer with a $2–5 million exchange, a distressed Orlando multifamily or retail asset acquired at a 7.5%+ going-in yield — rather than a fully stabilized, institutional-grade asset at 5.25% — is a legitimately superior risk-adjusted outcome. The distress discount compensates for the additional execution risk, provided the buyer has local market knowledge and operational capacity.

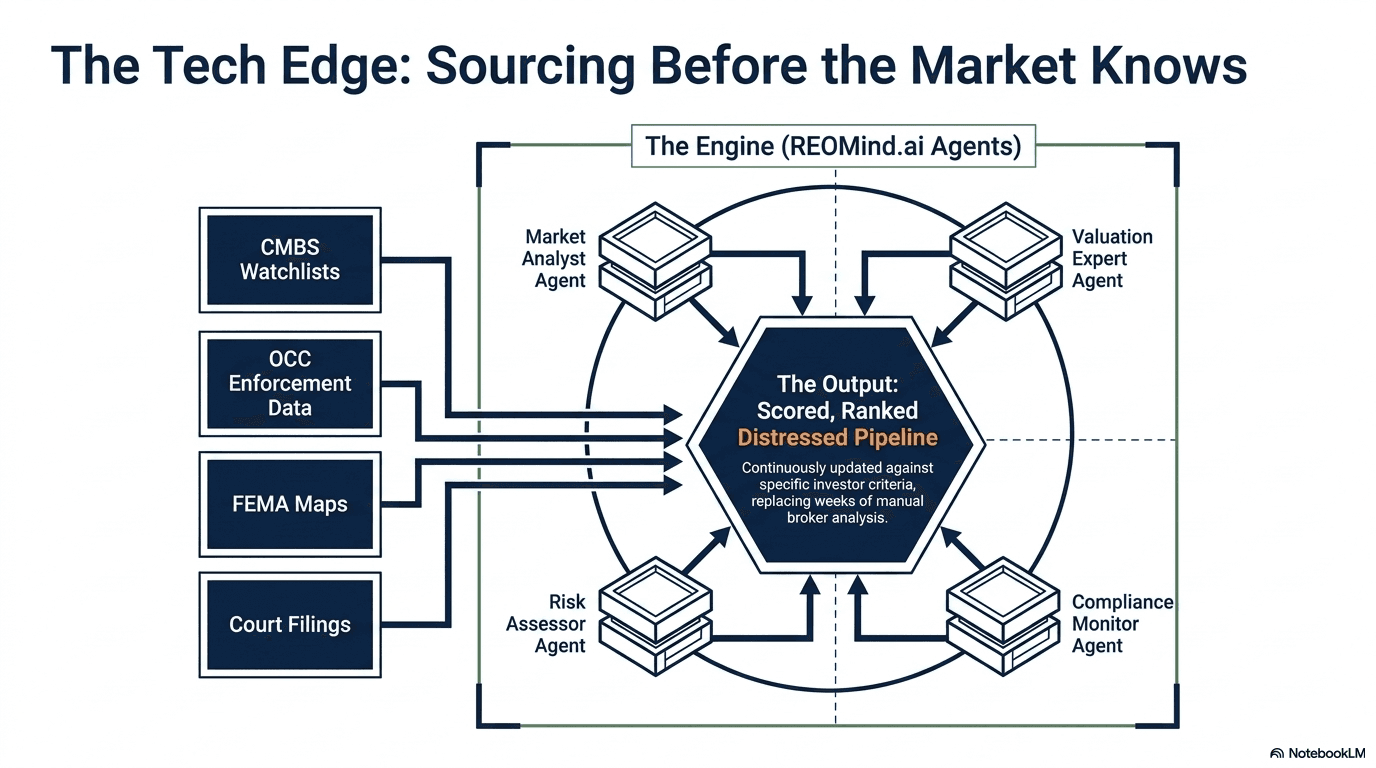

The REOMind.ai Advantage in a Data-Dense Market

Identifying the right distressed asset in a market with thousands of candidates requires a level of data processing that human-only analysis cannot sustain. This is precisely the context in which the REOMind.ai platform — developed through Linton Global Technologies and operating across the Florida CRE market — delivers a material competitive advantage.

The platform's Market Analyst Agent, Valuation Expert Agent, Compliance Monitor Agent, Investor Matcher Agent, and Risk Assessor Agent operate in concert to score distressed assets across dimensions that a traditional broker-driven process would take weeks to evaluate. The system cross-references CMBS servicer watchlists, OCC enforcement data, county court foreclosure filings, FEMA flood zone designations, insurance market pricing, and comparable sales data — producing a distress score and recommended acquisition structure for each target asset. The result is a pipeline that can be continuously monitored and filtered against investor-specific return criteria, rather than reactively chasing individual opportunities.

For institutional clients working with Linton Global Solutions, that translates to a shorter diligence timeline, a lower cost of acquisition discovery, and — critically — the ability to act before a property is broadly marketed. In the current cycle, the difference between a 68-cent note acquisition and a 78-cent acquisition is often a matter of days in execution speed.

Get the next Florida CRE report.

Cap rates, absorption, distress watch — delivered when it ships. No spam.

Due Diligence Priorities for Distressed Florida CRE

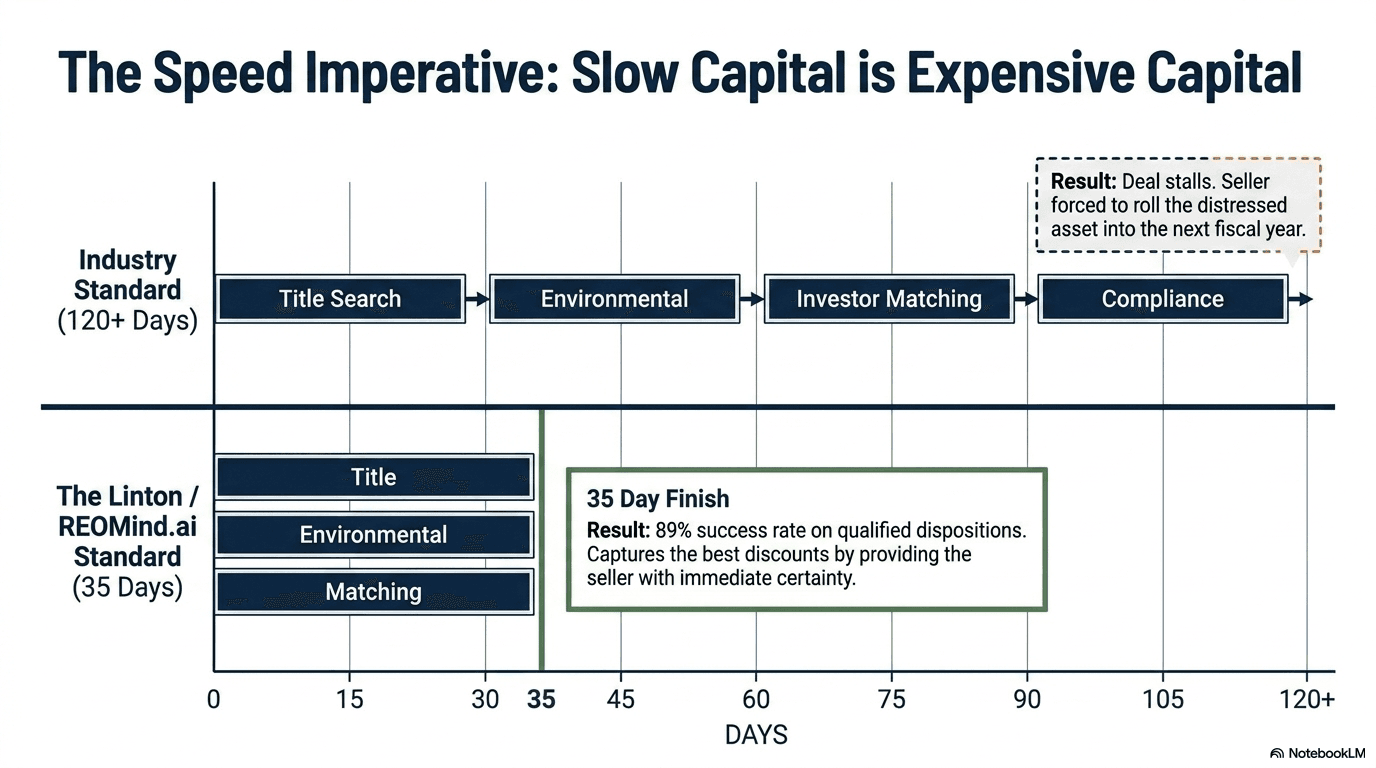

Distressed acquisitions compress timelines — sellers award deals to buyers who can close, not buyers who can negotiate the longest inspection period. That compression requires having your diligence framework pre-built before you begin looking at assets, not after you're under contract.

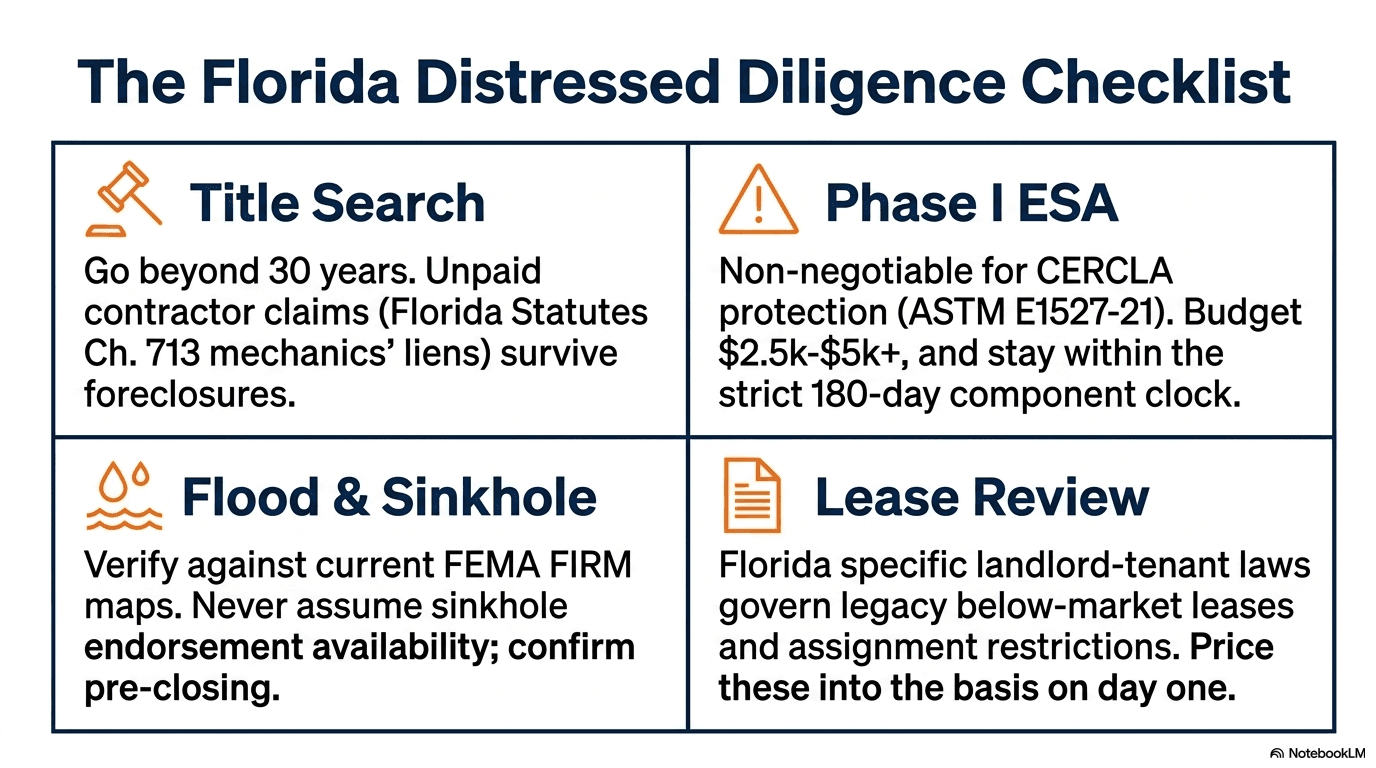

Title insurance is non-negotiable, and for distressed Florida assets, the search must go deeper than a standard 30-year chain. Mechanics' and materialmen's liens under Florida Statutes Chapter 713 attach to the property regardless of whether the lien is recorded before or after a mortgage — and unpaid contractor claims from a distressed owner's deferred maintenance program can survive a foreclosure in ways that will surprise buyers who rely solely on a standard title commitment. Engage a Florida construction lien attorney to review any property that has had capital work in the past 12 months.

Phase I ESA completed under ASTM E1527-21 is required for CERCLA “innocent landowner” protection and for any institutional lender's underwriting package. Budget $2,500–$5,000 for standard commercial assets; double that budget for industrial, self-storage (particularly those converted from gas station or automotive sites), and older hospitality properties with underground storage tank history.

Flood zone verification against current FEMA FIRM maps — not the borrower's representations — is essential. Sinkhole endorsement availability must be confirmed with the insurance market before closing, not assumed. In Orange and Hillsborough counties, a Phase I geotechnical review may be warranted on older masonry structures. These are not hypothetical risks; they are underwriting line items that change deal economics materially.

Finally, lease-by-lease review with a Florida real estate attorney matters in ways that differ from other states. Florida landlord-tenant law has specific provisions around commercial lease enforcement, assignment rights, and security deposit handling that can affect a distressed buyer's ability to re-tenant quickly. If the asset carries legacy leases with below-market rents or assignment restrictions, that must be priced into acquisition basis — not discovered at stabilization.

What a Compressed Disposition Cycle Looks Like in Practice

The conventional CRE disposition timeline — 120+ days from engagement to close — is a liability in a distressed market where lender motivation, competing buyer interest, and legal process windows are time-sensitive. The REOMind.ai platform was developed specifically to compress that timeline to approximately 35 days for properly prepared sellers, with an 89% success rate on qualified disposition engagements.

That compression comes from parallel-processing work that sequential brokerages handle in series: simultaneous title search, environmental screening, investor matching, and compliance verification running in the background while the deal is being structured, not after. For community banks and servicers with REO inventory they need to move before year-end — particularly given the Q4 2026 CMBS maturity concentration — a 35-day disposition cycle versus a 120-day cycle is not a minor operational improvement. It represents the difference between booking a loss in this fiscal year versus rolling the problem forward.

For buyers, the implication is reciprocal: capital that is positioned to close quickly — with lender pre-approvals or proof of funds in place, due diligence teams on retainer, and deal structures pre-negotiated — will consistently win the best distressed assets at the best pricing. Slow capital is expensive capital in this market.

Ready to Act Before the Q4 2026 Maturity Spike?

With 40% of 2026 CMBS maturities hitting in Q4, the window to acquire the best distressed assets at peak discount is now — not after they're broadly marketed. Michael R. Linton and Linton Global Solutions provide institutional-grade deal intelligence and execution for buyers across the I-4 corridor.

Schedule Your Distressed Asset Consultation →1031 Buyers and Family Offices: Sizing the Window

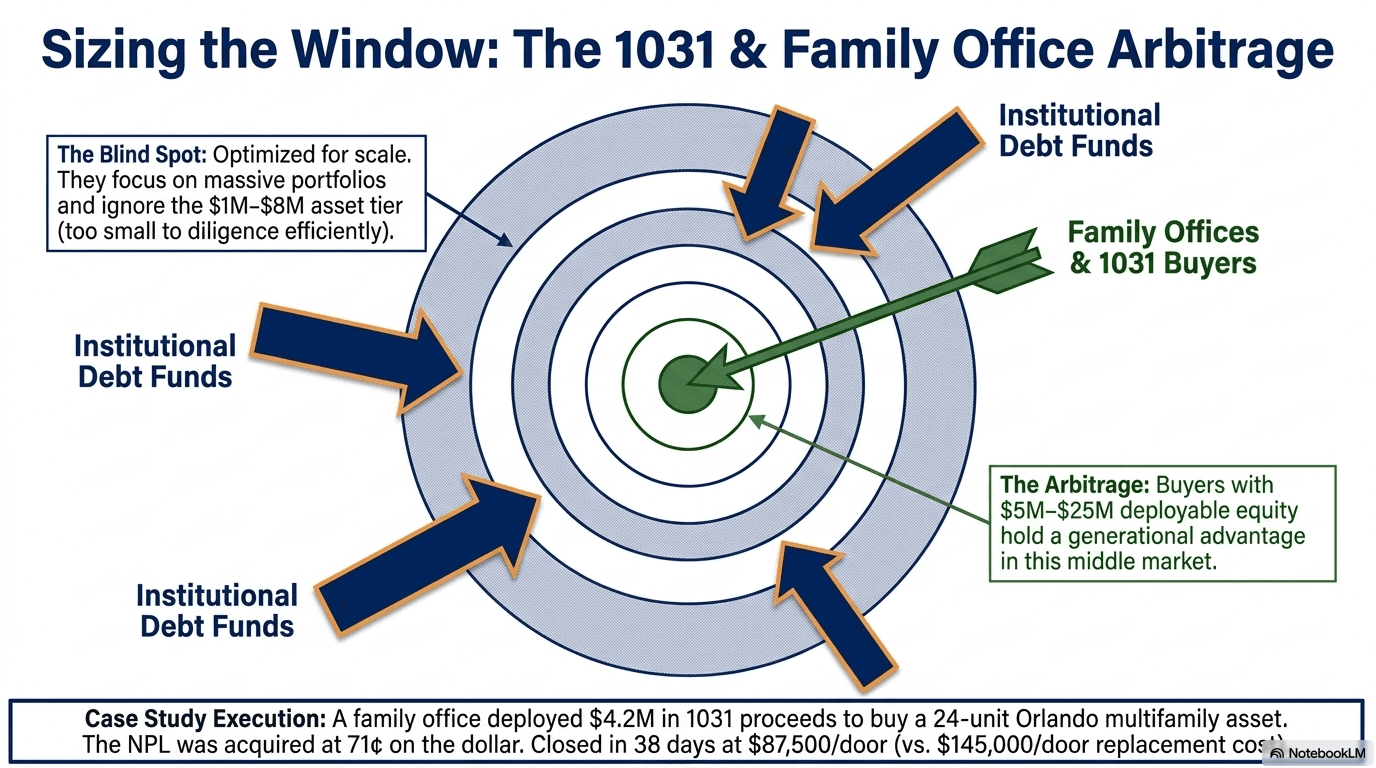

The 2026–2028 maturity wave is producing a generational buying window for non-institutional capital that has historically been priced out of distressed commercial transactions. Family offices with $5–25 million in deployable equity and 1031 exchange buyers coming out of appreciated residential or commercial positions are well-positioned to acquire assets that were previously only accessible to institutional debt funds.

The arbitrage is straightforward: institutional debt funds are optimized for scale and speed, which means they will focus on portfolio acquisitions and larger single-asset trades. The $1–8 million distressed asset — the office building in Longwood, the strip center in Kissimmee, the hospitality-adjacent retail pad in Sanford — is too small for most funds to diligence efficiently. That leaves a competitive gap that sophisticated local and regional buyers can exploit, provided they have market intelligence, legal infrastructure, and capital structure in place.

The 45/180-day 1031 exchange window is both a constraint and a competitive weapon. A motivated 1031 buyer who can close in 30–45 days is offering a distressed seller something that a fund running a 90-day REIT approval process cannot. In a judicial foreclosure state where sellers are trying to avoid lengthy workouts, that closing speed translates directly into acquisition price concessions of 5–15%.

A family office with $4.2M in 1031 exchange proceeds from the sale of a Tampa industrial portfolio was able to identify and close on a 24-unit Orlando multifamily asset — previously CMBS-financed at a 3.8% rate, now in special servicing — at a basis of $87,500 per door, against a replacement cost of $145,000 per door. The discounted note was acquired at 71 cents on the dollar by a debt fund, which then accepted the family office as the buyer at a still-discounted price to avoid judicial foreclosure. Closing occurred 38 days after initial contact. This is the 2026 playbook.

Key Takeaways

Frequently Asked Questions

What is the "maturity wall" and why does it matter for Orlando buyers in 2026?

The maturity wall refers to the concentrated mass of commercial real estate loans coming due within a compressed timeframe. Approximately $930 billion in CRE loans mature in 2026 alone — many originated at 3–4% rates that no longer pencil at today’s 6–7% refinancing environment. For Orlando buyers, this means a growing supply of motivated sellers, discounted note opportunities, and REO inventory across office, multifamily, retail, and hospitality that simply did not exist two years ago.

How does Florida's judicial foreclosure process affect distressed CRE acquisition timelines?

Florida is a judicial foreclosure state, meaning lenders must file a civil lawsuit and obtain a court judgment before conducting a foreclosure sale — a process that typically runs 12–18 months in contested cases. For buyers, this creates extended carrying-cost periods when acquiring NPLs, but it also creates leverage to negotiate deed-in-lieu agreements with borrowers who want to avoid public foreclosure. The key is building the judicial timeline into your underwriting model from day one, not treating it as a surprise.

What cap rates should investors target on distressed Orlando CRE in 2026?

Stabilized cap rates on quality Central Florida assets run 5.25–7.5% depending on asset class, with industrial and NNN retail at the tighter end and office and unanchored retail at the wider end. Distressed acquisitions — whether as direct REO purchases or note buys — should target 150–300 basis points above stabilized comps to compensate for execution risk, carrying costs, and repositioning capital. A distressed Orlando multifamily acquisition at an 8.0–8.5% going-in yield on current cash flow is a reasonable institutional target if occupancy and submarket fundamentals support it.

How does Florida's insurance crisis affect distressed CRE underwriting?

For properties carrying legacy insurance contracts written at 2019–2021 rates, renewal pricing is the biggest single NOI risk in the current underwriting environment. Commercial policies have surged over 200% at renewal for some Central Florida assets. Every distressed acquisition analysis must include an independent insurance market check — not a broker estimate — to determine current-market premium cost before finalizing the acquisition basis. Properties in flood zones or with sinkhole exposure require additional specialty endorsements that further compress NOI.

What is the documentary stamp tax obligation on a distressed Florida CRE purchase?

Florida imposes $0.70 per $100 of consideration (or fraction thereof) on deed transfers in all counties except Miami-Dade. On a $10 million acquisition, that is $70,000 due at recording. Mortgage documentary stamps run $0.35 per $100 of indebtedness. For note acquisitions structured as loan purchases followed by deed-in-lieu, the tax analysis is more nuanced — the discharged indebtedness in a deed-in-lieu transfer is treated as consideration, which has direct stamp tax implications. Florida real estate tax counsel should be engaged on any complex distressed transaction.

How can REOMind.ai and Linton Global Solutions help buyers source distressed Orlando CRE before it hits the market?

The REOMind.ai platform continuously monitors CMBS servicer watchlists, county foreclosure filings, OCC bank call reports, and off-market bank REO inventory across the I-4 corridor — producing a scored, ranked pipeline of distressed acquisition targets updated in near-real-time. Linton Global Solutions pairs that data infrastructure with 39 years of direct lender relationships at Florida community banks, credit unions, and servicers, providing buyers access to note sale and REO opportunities that never reach public marketing. The combination of AI-driven sourcing and relationship-based execution is the competitive edge in the current cycle.

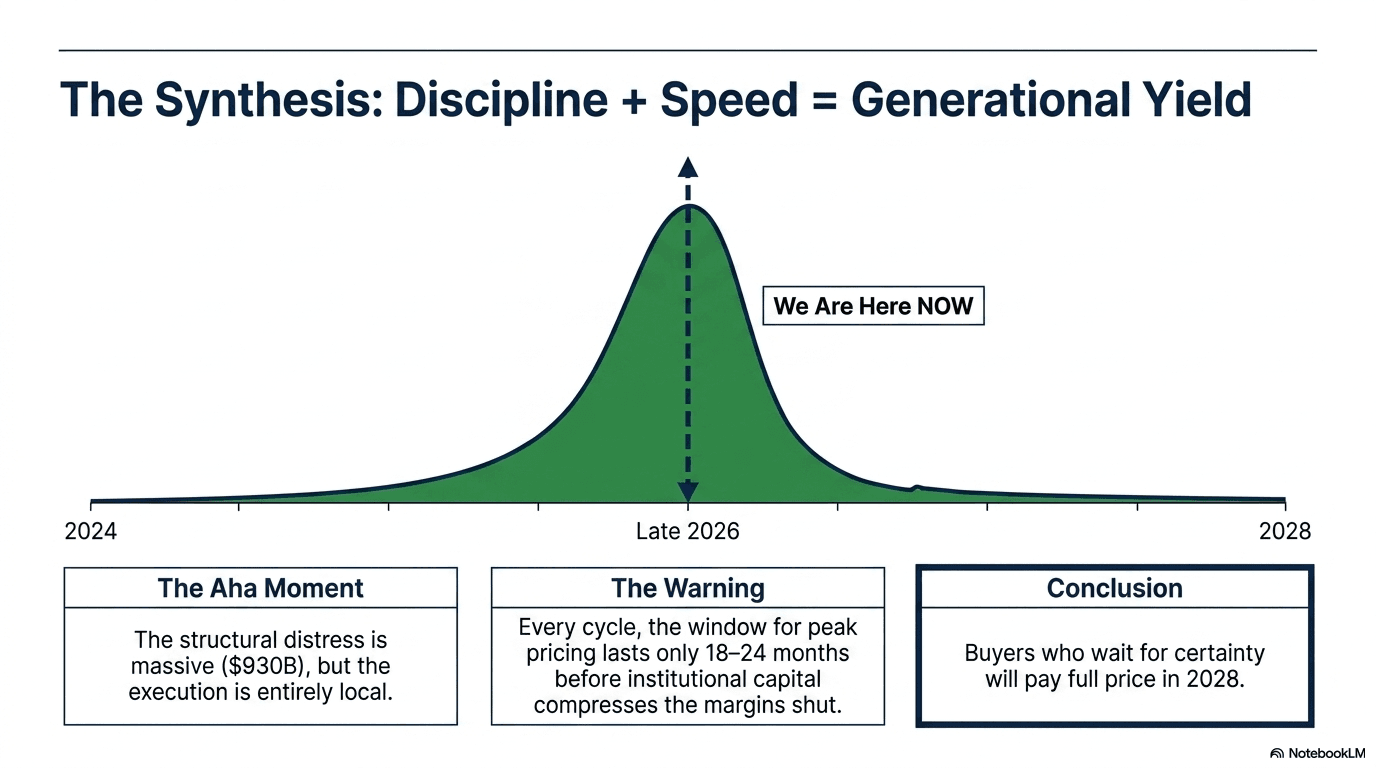

I've been doing this for 39 years, and I've watched three major distressed cycles from the inside — the S&L resolution, the GFC, and now this. Every cycle, the window for the best pricing lasts 18–24 months before institutional capital compresses it shut. We are in that window right now, and I am not being dramatic when I say the I-4 corridor has more quality distressed commercial inventory available at better pricing than I have seen since 2010–2011. The investors who move with discipline — proper diligence, clean capital, fast execution — will look back on this period as the best buying environment of their careers. The ones who wait for certainty will pay full price in 2028 and wonder what happened.

— Michael R. Linton, FL Broker #BK703722, NCREA, CREIPS, REALTOR®, 39 years Florida CRE

Works Cited

- ForvisMazars US. “Navigating Distressed Properties in Commercial Real Estate.” forvismazars.us, https://www.forvismazars.us/forsights/2026/03/navigating-distressed-properties-in-commercial-real-estate

- Morningstar DBRS. “U.S. CRE 2026 Outlook: Momentum Is Healthy, but Office Dynamics Remain Challenged.” dbrs.morningstar.com, https://dbrs.morningstar.com/research/471472

- Lee & Associates Central Florida. “Q1 2026 Industrial Market Report — Central Florida.” lee-associates.com, https://www.lee-associates.com/centralflorida/2026/04/24/

- Newmark. “Orlando Real Estate Market Report.” nmrk.com, https://www.nmrk.com/insights/market-report/orlando-real-estate-market-report

- Florida Department of Revenue. “Documentary Stamp Tax.” floridarevenue.com, https://floridarevenue.com/taxes/taxesfees/Pages/doc_stamp.aspx